Top 6 P&C KPIs and How Digitization Can Help You Meet Them

By Leor Melamedov

Property and casualty (P&C) insurance companies are increasingly aware that digital transformation will help them stay relevant and competitive into the future. There is often an understanding that automating insurance processes can improve customer experience and reduce costs. Yet digitizing, done correctly, also has a positive effect on a far wider range of KPIs that directly impact insurers’ bottom lines.

In this post, we’ll explore why the customer-facing processes may be the best starting point for insurance companies getting serious about digital transformation, and some of the top KPIs that can expect a boost from the adoption of new customer-facing technology.

Why digitize insurance processes on the frontend?

Digitization efforts tend to fall into one of two broad categories: frontend, customer-facing operations, and backend IT systems.

Insurance companies with unlimited budgets, staffing, and time can and should immediately start tackling both. Of course, most insurance companies only have so many resources they can devote to digitizing in any given year. While eventually, it’s important for both the backend and customer-facing interfaces to be automated and digitized, updating interfaces may bring a more immediate ROI at a lower cost.

Consider, for example, that the largest insurers plan on spending between $10 million to $20 million each year on robotic process automation (RPA) systems. These RPA systems automate repetitive back-office tasks related to underwriting, claims processing, and servicing via software bots.

While they serve a very important purpose, RPA systems require a huge investment of time and money. Furthermore, they do not directly address the problem of outdated customer-facing processes that lead to prolonged time to settlement, excessive touchpoints, endless back-and-forth with customers, error-filled FNOL reports, and other KPI-killers that plague insurance companies.

And now with the coronavirus increasing consumer demand for remote, digital insurance transactions, there has never been a better time to digitize these processes.

Here are just some of the KPIs that can be boosted quickly by prioritizing the adoption of frontend technology:

Revenue per policyholder

What it is: Revenue per policyholder, also known as revenue per customer, measures the amount of revenue generated per policyholder. Having consistent revenue per policyholder depends on two factors: Getting prospective customers to buy insurance policies, and retaining existing customers.

How digitization helps: Digitized customer sales journeys that include capabilities such as eForms, digital document collection, and mobile payments all facilitate successful onboarding. Agents that can sell policies over the phone while their customers instantly send over the necessary documents via mobile are able to close deals without friction and when interest is highest.

In addition to higher conversion rates, agents selling insurance remotely can reach more prospects in a more condensed amount of time compared to face-to-face sales.

However, new sales are not the only factor that impact revenue per policyholder. Retention is a big factor as well, and loyal customers bring dependable annual income for insurers.

Ensuring both new sales and retention is key for meeting this KPI, and digitization of processes makes it easier to both win new customers (new revenue streams) and keep existing customers (current revenue streams).

2. Average cost per claim

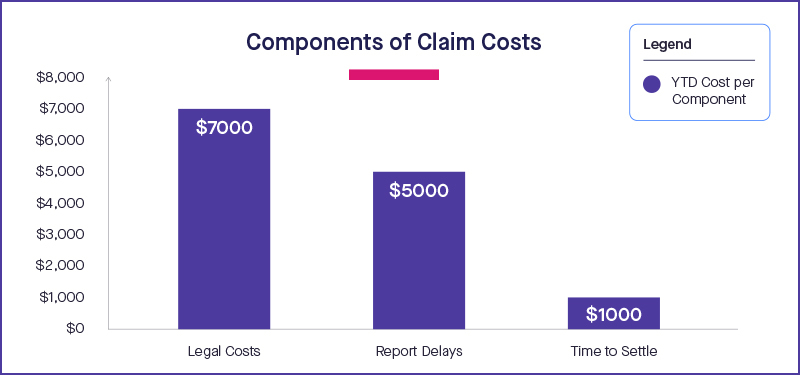

Controllable aspects of the claims process add to the average cost per claim.Source: Guiding MetricsWhat it is: The average cost per claim are the total costs associated with processing a claim, including legal costs, manpower hours, processing costs, and overhead. It doesn’t include the claims losses paid to policyholders.

How digitization helps: Inefficiencies and delays within the claims process can significantly increase the average cost per claim. Chasing customers for physical forms, documents, and evidence is extremely time-consuming, and therefore costly.

Non-digital forms also have a higher probability of containing errors or omissions that require customers to re-print, fill out, and send to the insurance company. The average cost to rework a claim is $25, which can add up to thousands of dollars in wasted funds per month.

On the other hand, digital customer-facing processes make it easy to instantly update forms with new or corrected information. Once the FNOL is in the electronic system, steps in the claims process can be easily consolidated and expedited to minimize overhead.

3. Average time to settlement

What it is: Average time to settlement is the length of time that elapses between FNOL and final claims payout. It has a significant effect on overall customer satisfaction, loyalty, and cost-effectiveness.

How digitization helps: Requiring customers to access a computer, printer, scanner, or fax when they need to provide their FNOL or additional documentation leads claims to drag on.

That’s not the case with digitization. Customers can simply take a photo or video of the damages and fill out mobile-optimized FNOL reports right at the scene of the incident. This can then be shared instantly with the insurer, who can provide guidance or correct errors in real-time. Rework, back-and-forths, and lags in communication are eliminated.

Finally, the payout can be issued via push-to-debit solutions, reducing the inefficiency inherent to sending checks and wire transfers.

While streamlined customer-facing solutions directly improve the speed of customer-facing claims steps, they also help expedite back-office processes. Customer-facing tech can sync with backend systems via API to eliminate manual data entry. Agents, adjusters claims assessors, surveyors, and any other party involved can instantly see customers’ electronic forms and evidence, and take action.

4. Loss ratio

What it is: The loss ratio is the cost of insurance claims paid plus adjustment expenses divided by the total amount of premiums earned. For instance, if an insurer pays $90 in claims for every $170 in premiums collected, the loss ratio would be 53%.

How digitization helps: Insurance companies need to ensure they are consistently earning more from income derived from premiums compared to losses incurred from claims payouts. If premiums fail to sufficiently cover claims losses, insurers will need to increase the price of their premiums.

While it’s best to avoid getting to the point where insurance premiums need to be hiked up, better customer-facing technological processes can make it more likely that policyholders will renew their policies despite higher costs. Medallia research found that among consumers who recently renewed a policy, even more cite liking or trusting the company as a reason to renew (47%) than price.

5. Retention and renewal

What it is: Retention refers to the number of customers who renew coverage after their initial term has passed. The average customer renewal rate is around 84%. While this may not sound bad, it represents a loss of 16% of premium-paying customers at the end of their term.

How digitization helps: According to Lynn Thomas, president at 21st Century Management Consulting, it costs seven to nine times more for an insurance agency to attract a new customer than to retain one. Therefore it behooves insurance companies to devote just as much, if not more attention to servicing, claims, and modifications as to sales.

A seamless digital claims and policy modification process ensure that customer satisfaction and even delight is guaranteed. Provided that rates are fair and agents are competent, digital transactions can help ensure customers stay with their provider for the long haul.

However, cumbersome or confusing digital tools are no better for customer loyalty than the outdated paperwork processes they are meant to replace. That’s why insurers seeking to boost customer retention through digitization should only adopt tools that are intuitive and easy to use.

Case in point: A recent McKinsey survey found that digitization in insurance increased by nearly 30% since the start of the coronavirus pandemic. However, customer satisfaction with digital tools was lowest in insurance compared to other industries. The number one reason for dissatisfaction? The pervasiveness of “hard to use [digital] tools.”

That’s why legacy digital tools that require access to computers and PDF readers, such as first-generation eSignature providers, can no longer be considered a helpful digital tool. On the other hand, mobile-optimized forms, documents, and signatures ensure technology is as frictionless and location-independent as possible.

6. New policy sales

What it is: New policy sales measures the number of new policies onboarded. It can be tracked per agent or per policy type.

How digitization helps: Provided that retention is maintained, each new policy signed is extremely lucrative and therefore worth fighting for. Consider that the average homeowner makes a claim every nine years, and motorists file insurance claims roughly once every 17.9 years. The vast majority of years policyholders will never make a claim — yet they will pay annual premiums. But if prospective customers fail to convert, all that potential income never materializes.

When customers shop for P&C insurance, they first check that a provider offers the type of plan they need and a good rate. But after that, their likelihood of actually signing a policy comes down to the ease and speed of completing the application.

Insurance providers that require face-to-face meetings, bounce prospective customers from channel to channel, prolong phone conversations, or require physical paperwork to be filled out jeopardize their deals with needless friction.

On the other hand, digitized eForms and eSignatures allow customers to complete their application via a smartphone interface while on a sales call. Agents can provide reassurance, answer questions, and ensure everything is filled out correctly the first time. A smooth onboarding and sales process doesn’t just make a good first impression — it’s good business.

Digital customer interface as a fast way to reach KPIs

Insurance companies can quickly start seeing a lift in their most important KPIs by adopting digital interface technology. Digitized customer journeys touch every aspect of the business, many of which insurers might not expect to see affected.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Source: Guiding Metrics

What it is: The average cost per claim are the total costs associated with processing a claim, including legal costs, manpower hours, processing costs, and overhead. It doesn’t include the claims losses paid to policyholders.

How digitization helps: Inefficiencies and delays within the claims process can significantly increase the average cost per claim. Chasing customers for physical forms, documents, and evidence is extremely time-consuming, and therefore costly.

Non-digital forms also have a higher probability of containing errors or omissions that require customers to re-print, fill out, and send to the insurance company. The average cost to rework a claim is $25, which can add up to thousands of dollars in wasted funds per month.

On the other hand, digital customer-facing processes make it easy to instantly update forms with new or corrected information. Once the FNOL is in the electronic system, steps in the claims process can be easily consolidated and expedited to minimize overhead.

Source: Guiding Metrics

What it is: The average cost per claim are the total costs associated with processing a claim, including legal costs, manpower hours, processing costs, and overhead. It doesn’t include the claims losses paid to policyholders.

How digitization helps: Inefficiencies and delays within the claims process can significantly increase the average cost per claim. Chasing customers for physical forms, documents, and evidence is extremely time-consuming, and therefore costly.

Non-digital forms also have a higher probability of containing errors or omissions that require customers to re-print, fill out, and send to the insurance company. The average cost to rework a claim is $25, which can add up to thousands of dollars in wasted funds per month.

On the other hand, digital customer-facing processes make it easy to instantly update forms with new or corrected information. Once the FNOL is in the electronic system, steps in the claims process can be easily consolidated and expedited to minimize overhead.