9 Actionable Ways Banks Can Drive Digital Transformation

By Leor Melamedov

In today's digital world, what bank wouldn’t want to be known as digital first?

Growing consumer demand for convenient mobile and online banking, combined with acceleration of remote interactions in light of COVID-19, has turned digital transformation into a popular buzzword.

But are banking executives putting their money where their mouth is?

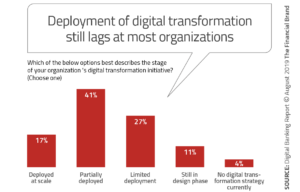

Studies suggest that many banks are still significantly behind customer expectations when it comes to implementing digital banking. According to the Innovation in Retail Banking 2019 Report, a mere 17% of financial institution executives say that their bank has deployed digital transformation initiatives at scale. A plurality (41%) say that they have only partially deployed transformative new technology.

Banking executives’ perceptions of their banks as being semi-digital jibes with consumers’ experiences. A Lightico study found that 62% of middle-income banking customers have been redirected to a physical branch when they attempted to complete a banking task online. Another 54% have been asked to print, sign, or email documents during an online banking journey.

Since many banks struggle to track the customer journey, they aren’t always aware of the gaps in their digital offerings. Here, we present the signs that a bank is doing well at digitization.

Signs of a Digital-First Bank

Lots of banks have a mobile app or website, but that doesn’t make them digital-first. These are some signs that a bank is truly committed to a digital transformation.

Adopt of Agile Principles

Today’s fastest-growing software companies have embraced Agile development principles, which allows teams to develop products using incremental work sequences known as “sprints.” This goes hand-in-hand with design thinking, which puts empathy for customers’ real wants and needs at the center of everything that’s being developed.

Digital-first banks embrace these methodologies, building roadmaps that solve for customers’ actual problems and working in highly efficient ways.

2. Prioritize Front-End Systems

Banking regulations have a way of leading to cumbersome processes and paperwork. But it doesn’t need to be that way. In fact, it shouldn’t.

Banks are first and foremost service providers, so it’s key that they prioritize tools, technologies, and services that directly impact their customer’ experience. Digital-first banks know that they’ll see a large ROI from investing in front-end systems that improve the customer’s digital experience. Faster turnaround time, improved agent satisfaction, and greater customer loyalty can all be expected outcomes.

3. Start With a Minimum Viable Product (MVP)

Here’s another approach taken from the world of fast-growing start-ups. A Minimum Viable Product (MVP) is a technique that allows developers to roll out an initial version of a product, completing the final version only after receiving feedback from initial users. Digital-first banks know that testing ideas quickly before the general release leads to more successful outcomes.

4. Let Customer Journeys be the Guide

Digital-first banks know that analyzing their customers’ journeys is one of the best ways to identify digital gaps and areas for improvement. They first decide on the most common tasks that customers want to accomplish, and then run customer journey mapping tools or collect real-time customer feedback to pinpoint where customers are most likely to drop out of the journey or face frustration. It’s critical that mapping customer journeys produces highly detailed results that cross-functional teams can act upon.

5. Break Down Initiatives

Digital transformation often sounds intimidating and overwhelming when discussed in general terms. That’s why digital-first banks know to break general goals into specific initiatives, with those initiatives broken down into even more specific tasks. Aside from making new initiatives more manageable to tackle, this allows for easier delegation to different teams, from developers to customer-facing employees to C-level executives.

Whether a team is responsible for developing a solution, approving a solution, or educating customers about a solution, everyone should know what their role is.

6. Plan Cross-functional Roadmaps

New and future initiatives should be planned by mapping customer journeys, such as new account opening, bank transfers, credit card applications, and complaint resolution. Many digital-first banks divide digital initiatives into products that are each assigned a cross-functional working group spearheaded by a product owner.

In addition to making sure teams are effectively working together, effective digital-first banks ensure dependencies for these initiatives are accounted for. This encourages cross-functional teams to coordinate efforts and prevents bottlenecks.

Finally, digital-first banks should break down the resources they need to accomplish each initiative in the roadmap. Categories include goals, budget, project owner, technology, and KPIs.

7. Make Smarter Decisions on Which Initiatives to Pursue

Banks that have a successful digital program carefully evaluate which initiatives are worth pursuing. They typically look at three factors that influence an initiative’s potential: value to customers, impact on business, and feasibility. Does it improve the customer experience? Would it likely have a direct positive impact on the bank’s financial goals? And does the bank have the right resources in place (e.g., manpower, budget, stakeholder-buy-in) to increase the initiative’s likelihood of success? These three overarching factors are critical to have in place before taking a step further.

8. Stay Ahead of the Curve

Let’s face it: It’s not easy for traditional banks to keep up with the neobanks and fintechs of the world when it comes to anticipating digital trends. But leading digital-first banks are giving neobanks a run for their money by using future-state mapping for customer journeys.

They imagine the future of the customer journey in say, four to five years’ time, and then develop a minimal viable product (MVP) that can be launched in less than a year that satisfies that vision.

Future-state mapping allows banks to not just anticipate consumer trends, but easily make adjustments to new products based on customer feedback and behavior. Predict, test, learn.

9. Find (and Pick) Low-Hanging Fruit

The top digital-first banks plan for large and long-term projects. But they also know how to spot opportunities for quick wins that are easier to implement and require fewer resources. These are an important addition to banks’ product roadmaps because they allow stakeholders to immediately see value from digital initiatives. Success with these projects will lead to stakeholders showing more enthusiasm for more complex projects in the future.

The Bottom Line

A financial institution doesn’t need to be a neobank or fintech startup to be digital-first. It’s time that traditional banks go beyond partial measures and enact the full digital transformation they need to stay relevant in the 21st century. By using Agile methodologies, mapping the full digital customer journey, and bringing together cross-functional teams, they can see greater value from digital initiatives.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Banking executives’ perceptions of their banks as being semi-digital jibes with consumers’ experiences. A Lightico study found that 62% of middle-income banking customers have been redirected to a physical branch when they attempted to complete a banking task online. Another 54% have been asked to print, sign, or email documents during an online banking journey.

Since many banks struggle to track the customer journey, they aren’t always aware of the gaps in their digital offerings. Here, we present the signs that a bank is doing well at digitization.

Banking executives’ perceptions of their banks as being semi-digital jibes with consumers’ experiences. A Lightico study found that 62% of middle-income banking customers have been redirected to a physical branch when they attempted to complete a banking task online. Another 54% have been asked to print, sign, or email documents during an online banking journey.

Since many banks struggle to track the customer journey, they aren’t always aware of the gaps in their digital offerings. Here, we present the signs that a bank is doing well at digitization.