Leverage Digital Completion across multiple communication channels to offer more rapid feedback and document collection, eSignature support, confirmation of receipt, and more.

The Customer Pain

Disagreements between customers and banks require clarification, but the process of getting that clarification is difficult.

Customers are often forced to work outside their channel of choice when trying to file a dispute with their bank.

For example, they may find themselves attempting to complete the process on their phone, but end up getting redirected to a physical branch.

Submitting proof of the issue or signing forms involves multiple steps.

As a result of these service-level issues, customers are at risk of escalating their cases, getting entangled in legal disputes, and even churning.

The Bank Pain

Disjointed processes lead to a proliferation of open cases that languish and lag.

Valuable employee time is wasted on multiple or incremental contacts with customers.

Lengthy turnaround time leads to serious service-level issues.

How to Digitally Complete Dispute Resolution

Step 1: Customer engages (visits bank branch, calls contact center, uses online chat, visits website, etc.) and begins a dispute process. This can be agent-assisted (through a conversation with a rep), or workflow-driven (via web/portal).

Step 2: Bank verifies the customer’s identity using digital ID verification software, one-time password (OTP), or knowledge-based authentication depending on the channel and whether it’s behind an authenticated space.

Step 3: The digital dispute form is collected (if necessary). Supporting documentation/proof related to the dispute is also collected. If agent-assisted, the dispute form can be reviewed in real time using shared review. All documentation appears on the agent side (branch/call center).

Step 4: Bank launches an internal investigation executed (via the standard process). Communication/updates can be pushed to the customer (manually or via API integration).

Step 5: Dispute resolution achieved and communicated back to the customer. Acknowledge resolution response to customer –– ensuring that communication was received.

Results

Improved First-call Resolution (FCR)

Improved Turnaround time (TAT) (especially with digital document collection)

Improved overall time to resolution

Improved Net Promoter Score (NPS) / Customer Satisfaction Score (CSAT)

Fraud victims are under enough stress. Banks have an invaluable opportunity to alleviate that stress by speeding up and streamlining fraud investigation journeys. A seamless automated digital workflow improves the customer experience in banking during fraud investigations.A Digital Completion platform also comes with a full audit trail/documentation trail and a more secure “proof” of receipt than legacy processes such as mail and fax — where additional touchpoints can result in lost or misrouted communications.

The Customer Pain

Customer fraud complaints are serious and require investigation, but the process of investigation can be fraught with inconvenience

When filing fraud complaints, banking customers are often forced to work outside their channel of choice

Submitting proof or signing forms is annoying and submission back is problematic

Fraud journeys may require additional information or supporting documentation and notarization of specific forms –– which can be a customer inconvenience

All this makes for a high-stress experience for customers who may be a victim of fraud

The Bank Pain

Longer time to resolve a dispute

False starts or open cases that lag

Insufficient documentation or responses –– resulting in multiple contacts/incremental contacts with customers

Extra steps lead to long turnaround times, which in turn leads to serious service-level issues such as escalation and churn

How to Digitally Resolve Fraud Incidents

Step 1: The customer engages (via phone call, chat, web, etc.) and begins a fraud investigation request (can be agent-assisted or workflow-driven).

Step 2: Bank verifies the customer’s identity using digital ID verification software, one-time password (OTP), or knowledge-based authentication depending on the channel and whether it’s behind an authenticated space.

Step 3: Applicable fraud forms and supporting documentation is requested or sent to the customer to complete. If the fraud case is agent-assisted, these documents can be co-reviewed via digital channels using the shared review capability.

Step 4: The bank conducts an internal investigation. During this time, additional digital document collection or eForms may be required ( affidavits, police reports, etc.).

Step 5: The fraud dispute is resolved and findings are securely communicated to the customer (with acknowledgment possible).

Results

Improved FCR

Improved TAT (especially with digital document collection)

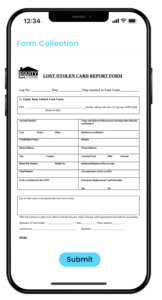

While many banks already have a system in place that allows customers to digitally report lost or stolen credit cards, a Digital Completion platform can assist in cases where any supporting documentation or follow-up is required (e.g. should it move to a fraud or dispute process).

The Customer Pain

When reporting a lost or stolen credit card, banking customers are often forced to work outside their channel of choice

Submitting proof or signing forms is frustrating and submission back may be slow

The Bank Pain

Banks often have developed a quick reporting process for this solution (such as a contact center that fields calls) but any additional reporting or documentation may still require a lengthy process to complete

Lengthy processes result in lost employee time and wasted resources

How to Digitally Collect Lost and Stolen Credit Card Reports

Step 1: The customer engages (via phone call, chat, web, etc.) and reports a lost or stolen credit card (can be agent-assisted or workflow-driven).

Step 2: Bank verifies the customer’s identity using digital ID verification software, one-time password (OTP), or knowledge-based authentication depending on the channel and whether it’s behind an authenticated space.

Step 3: To supplement existing processes, a digital workflow allows banks to collect specific information, address key questions, and/or validate last-known purchases, etc. a Digital Completion platform also assists in collecting data to verify if possible fraud has also occurred.

Step 4: Standard bank processing for lost/stolen cards. If fraud is suspected, an interactive session can be activated for the fraud processing flow.

Step 5: A new account number is issued, and any disputed charges or events are resolved and communicated back to the customer.

Results

Improved FCR

Improved TAT (especially with digital document collection)

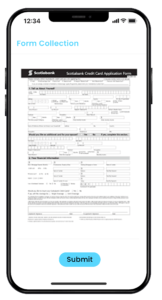

Not all banks have a robust online account servicing process. That’s OK. Such banks can still leverage a Digital Completion platform to digitize the replacement or issuing of credit cards.This improves customer-facing credit card processes via automated workflows to help identify higher-risk scenarios via self-service channels.For example, if a customer still has the card in their possession but it is just damaged, that can trigger a simple credit card replacement workflow. If a customer is reporting a lost or stolen credit card, that comes with a higher level of risk and requires an investigation workflow to be activated.

The Customer Pain

Customers are forced to go through manual processes or fulfill time-consuming requirements to request additional/authorized users

Customers are forced outside their channel of choice or require time to engage when the branch is open –– versus being able to engage from any location or on their own time

The Bank Pain

May not be able to engage customers outside of staffed hours for these types of requests

May require signed forms or processes not readily available online

How to Digitally Replace or Issue Additional Credit Cards

Step 1: The customer engages (via phone call, chat, web, etc.) and requests a replacement or additional credit or debit cards. This can be agent-assisted or workflow-driven.

Step 2: Bank verifies the customer’s identity using digital ID verification software, one-time password (OTP), or knowledge-based authentication depending on the channel and whether it’s behind an authenticated space.

Step 3: Authorization forms are collected to issue the new cards, or add authorized users to the accounts.

Step 4: Internal review and processing of requests is completed. Accounts are updated and new or replacement cards are sent to the customer.

Presidential and regulatory complaints occur when the customer has escalated an issue up to the highest internal escalation point. In other cases, they'll engage with regulators and/or other agencies regarding their issue. The customer is usually agitated and the situation may be heated.A Digital Completion platform can offer a solid audit trail for any and all documents shared during presidential/regulatory complaints, as well as real-time messaging with an agent. This allows for a formal and well-documented engagement process and provides an efficient way to communicate and share with customers.

The Customer Pain

Submitting proof or signing forms is often an annoying and complicated process

Lengthy turnaround time due to digital silos and legacy processes

The customer is already frustrated, and prolonged processes and delays only exacerbate that frustration

The Bank Pain

Communicating with customers is difficult to do both securely and efficiently

It requires a solid audit trail and documentation sharing

Regulatory investigations or challenges often spawn from this journey, putting efficiency at risk

How to Digitally Resolve Presidential/Regulatory Complaints

Step 1: The customer engages with the bank.

Step 2: The optional digital identity verification process is engaged.

Step 3: Additional documentation, supporting evidence, or content is shared in real time or via a workflow/standard requests.

Step 4: Throughout the investigation, the bank communicates with the customer. A shared digital review process can be used to walk the customer through any specific findings or clarification on documentation, if and when needed.

Step 5: The issue is resolved and communicated back to the customer.

Results

Improved TAT (especially with digital document collection)

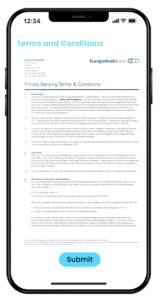

Spare your customers the headache of listening to tedious agent scripts with instant legal acknowledgments of terms and conditions. Get consent wherever your customers are.

The Customer Pain

Customers endure a cumbersome process for banking terms and conditions — they must give consent on hardcopies, or listen to lengthy agent scripts

Customers may receive multiple T&Cs during an engagement when just one blanket consent form would suffice

Customers are more likely to dispute verbal T&C engagements. In part, this is due to misunderstandings during verbal consent approvals.

The Bank Pain

If the T&Cs are verbal, it often takes more time –– and tracking/auditing those sessions requires call logging and archival research to extract

Verbal T&Cs may prolong AHT and lead to employee burnout due to the repetitive nature of these engagements

How to Digitally Complete Terms and Conditions

Step 1: The customer engages the bank from any channel

Step 2: Digital ID verification is optionally employed

Step 3: e-Consent is captured at the beginning of the interactive session, or via specific forms/consent requests, or via specific T&Cs associated with a new or existing product/service that demands a change in terms

Step 4: Customer consent is received for terms and conditions

Processes surrounding the Servicemembers Civil Relief Act (SCRA) are still stuck in the 1990s at best. A Digital Completion platform provides a streamlined and secure way to complete processes for troops and their families.

The Customer Pain

Servicemembers lack access to many banking communication channels

Servicemembers struggle to engage with bank employees during staffed hours as they may literally be on the other side of the world

Frustration is widespread due to old-school technology that even then isn't accessible to them

Servicemembers deal with enough stress already — they don't need a banking process that adds to it

The Bank Pain

SCRA means heavily regulated journeys: there’s a potential for fines, penalties, or bad press when it isn't managed effectively

Manual and complicated processes with major time gaps and delays in receiving documentation or contacting forward-deployed troops

Many other channels are less secure or not easily accessed.

How to Digitize SCRA Processes

Step 1: The customer engages from any channel

Step 2: Digital identity verification (optional) is employed

Step 3: Applicable documents captured (military orders, etc.) to complete account processing for SCRA impacted customers

Step 4: All processing/account updates are completed and communicated back to the customer as required

Results

Improved customer access

Improved FCR

Improved TAT (especially with document collection)

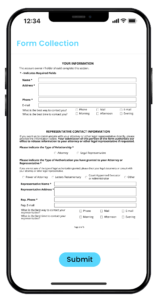

The transfer of bank accounts and assumption of accounts/debts/loans (generally in the case of death or divorce of the primary account owner(s)) is stressful as these transfers are typically for loved ones — and carries risk for the bank. Fixing broken customer journeys can ease the bureaucracy surrounding it.

The Customer Pain

The customer is often forced to work outside their channel of choice

The process of submitting forms is often annoying and complicated

Turnaround time and “gaps” in engagement due to the process and additional steps can cause delays

The customer lacks visibility into the process

The Bank Pain

Difficulty completing the process and/or challenges with all parties completing the process in a timely manner

Banks often rely on manual processes and/or engaging parties separately to complete those processes –– instead of in a joint/unified manner

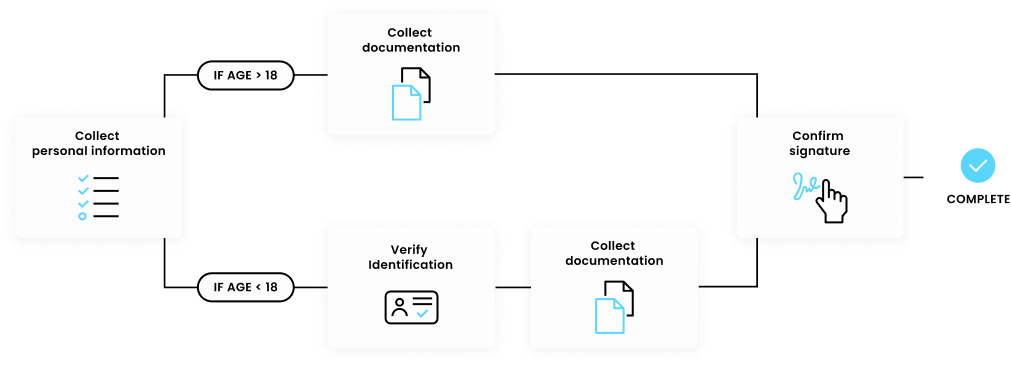

How to Digitize Account Transfers and Assumptions

Step 1: Customer engages from practically any channel

Step 2: The customer’s identity is verified using digital ID verification software, one-time password (OTP), or knowledge-based authentication depending on the channel and whether it’s behind an authenticated space

Step 3: Authorization eForms are collected from all impacted parties

Step 4: All processing/account updates are completed and communicated back to the customer as required

Results

Improved FCR

Improved TAT (especially through eForm collection)

With a Digital Completion platform, bank customers can access self-service workflows via the bank’s website or IVR. It’s a simple process via the Integration Hub, though more advanced options are available via client-developed API designs.Additional workflow options can be harnessed to streamline self-service journeys while still providing improved logic and guidance.

The Customer Pain

Customers may have very limited options to engage the bank online to complete forms or submit documents

Customers may be forced to engage in less desirable channels to complete a process –– including voice –– and need to complete processes on the bank’s schedule instead of their own

The Bank Pain

The bank’s infrastructure may not be up-to-date enough to support the automatic handling of requests

The bank may require staff to assist or support requests that often should not require up-front staffing to help a customer complete

How to Digitize Self-Service Workflows

Step 1: The customer and agent enter an interactive session through IVR, website engagement, or other self-service link option

Step 2: The bank provides the customer with the necessary eForms and document requests necessary to complete the process

Step 3: The customer sends the bank the completed eForm or document, which is then processed in the back office

Step 4: The process is completed (or issue resolved)

Results

Improved FCR

Easier document/form collection –– in the customer’s channel of choice

Reduced overhead on staff (no agent required)

Consistent compliance/user experience

The Bottom Line

Banks can complete more customer journeys, faster with a Digital Completion platform such as Lightico’s Digital Completion Cloud. By eliminating silos and replacing manual legacy processes with end-to-end digital journeys, practically any customer-facing process can be dramatically accelerated.

Try the Interactive Demo

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

While many banks already have a system in place that allows customers to digitally report lost or stolen credit cards, a Digital Completion platform can assist in cases where any supporting documentation or follow-up is required (e.g. should it move to a fraud or dispute process).

While many banks already have a system in place that allows customers to digitally report lost or stolen credit cards, a Digital Completion platform can assist in cases where any supporting documentation or follow-up is required (e.g. should it move to a fraud or dispute process).

Not all banks have a robust online account servicing process. That’s OK. Such banks can still leverage a Digital Completion platform to digitize the replacement or issuing of credit cards.

This improves customer-facing credit card processes via automated workflows to help identify higher-risk scenarios via self-service channels.

For example, if a customer still has the card in their possession but it is just damaged, that can trigger a simple credit card replacement workflow. If a customer is reporting a lost or stolen credit card, that comes with a higher level of risk and requires an investigation workflow to be activated.

Not all banks have a robust online account servicing process. That’s OK. Such banks can still leverage a Digital Completion platform to digitize the replacement or issuing of credit cards.

This improves customer-facing credit card processes via automated workflows to help identify higher-risk scenarios via self-service channels.

For example, if a customer still has the card in their possession but it is just damaged, that can trigger a simple credit card replacement workflow. If a customer is reporting a lost or stolen credit card, that comes with a higher level of risk and requires an investigation workflow to be activated.

Presidential and regulatory complaints occur when the customer has escalated an issue up to the highest internal escalation point. In other cases, they'll engage with regulators and/or other agencies regarding their issue. The customer is usually agitated and the situation may be heated.

A Digital Completion platform can offer a solid audit trail for any and all documents shared during presidential/regulatory complaints, as well as real-time messaging with an agent. This allows for a formal and well-documented engagement process and provides an efficient way to communicate and share with customers.

Presidential and regulatory complaints occur when the customer has escalated an issue up to the highest internal escalation point. In other cases, they'll engage with regulators and/or other agencies regarding their issue. The customer is usually agitated and the situation may be heated.

A Digital Completion platform can offer a solid audit trail for any and all documents shared during presidential/regulatory complaints, as well as real-time messaging with an agent. This allows for a formal and well-documented engagement process and provides an efficient way to communicate and share with customers.

Spare your customers the headache of listening to tedious agent scripts with instant legal acknowledgments of terms and conditions. Get consent wherever your customers are.

Spare your customers the headache of listening to tedious agent scripts with instant legal acknowledgments of terms and conditions. Get consent wherever your customers are.

Processes surrounding the Servicemembers Civil Relief Act (SCRA) are still stuck in the 1990s at best. A Digital Completion platform provides a streamlined and secure way to complete processes for troops and their families.

Processes surrounding the Servicemembers Civil Relief Act (SCRA) are still stuck in the 1990s at best. A Digital Completion platform provides a streamlined and secure way to complete processes for troops and their families.

The transfer of bank accounts and assumption of accounts/debts/loans (generally in the case of death or divorce of the primary account owner(s)) is stressful as these transfers are typically for loved ones — and carries risk for the bank. Fixing broken customer journeys can ease the bureaucracy surrounding it.

The transfer of bank accounts and assumption of accounts/debts/loans (generally in the case of death or divorce of the primary account owner(s)) is stressful as these transfers are typically for loved ones — and carries risk for the bank. Fixing broken customer journeys can ease the bureaucracy surrounding it.

With a Digital Completion platform, bank customers can access self-service workflows via the bank’s website or IVR. It’s a simple process via the Integration Hub, though more advanced options are available via client-developed API designs.

Additional workflow options can be harnessed to streamline self-service journeys while still providing improved logic and guidance.

With a Digital Completion platform, bank customers can access self-service workflows via the bank’s website or IVR. It’s a simple process via the Integration Hub, though more advanced options are available via client-developed API designs.

Additional workflow options can be harnessed to streamline self-service journeys while still providing improved logic and guidance.