Consumer Study Details How Traditional Banks Should View Digital-Only Banks

By Leor Melamedov

It’s a common perception that veers into tautology: all-digital banks, also known as neobanks, provide a more robust digital experience than traditional banks. A recent survey of 1,007 U.S. bank customers has confirmed this perception, particularly in the shadow of the “Great Lockdown” when digital, remote transactions became a matter of real urgency.

But perhaps even more interestingly, the survey reveals a clear correlation between a strong digital banking experience and a strong overall customer experience. By pouring most of their efforts and budget into digitized systems, digital-only banks enjoy dramatically higher customer satisfaction and loyalty than traditional financial institutions.

While traditional institutions won’t -– and shouldn’t — take this as their cue to abandon their physical branches, it does suggest that eliminating digital friction has a strong spillover effect on customers’ overall perception of their bank. And the reputational and financial rewards for improving CX cannot be overstated, especially in our competitive environment.

How digital-only vs. traditional banks stack up

Across the four major categories our survey studied — ease of digital onboarding, digital credit card application experience, customer satisfaction, and customer loyalty — digital-only banks came in at first place.

While the following results may be sobering for large and established institutions, the good news is that fully digitizing the front-end and ironing out kinks in the online customer journey can give traditional banks the edge they need to maintain their market dominance.

Seamless account onboarding

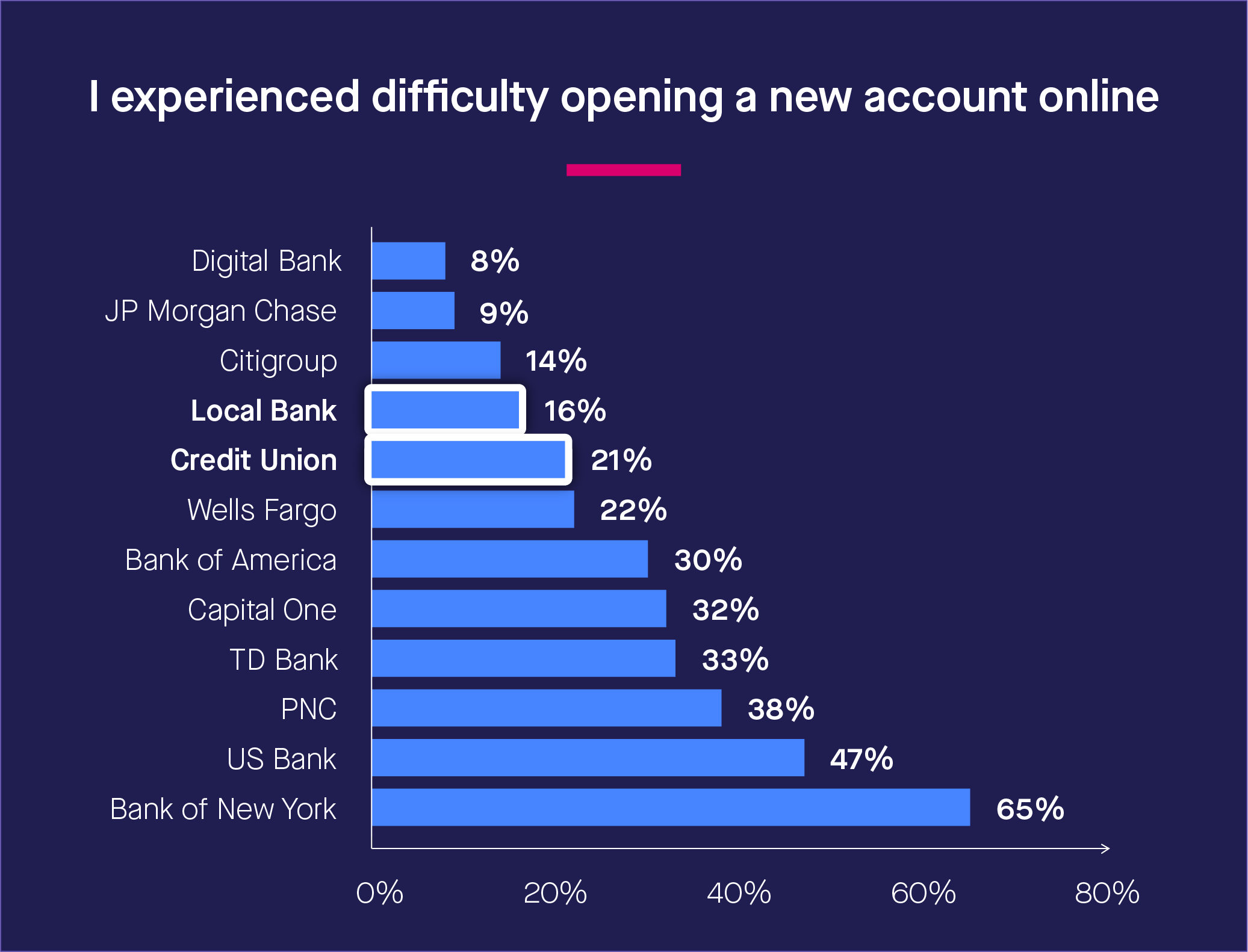

When customers attempt to open a bank account online, they intend to start and finish that process online. Unfortunately far too many customers of traditional banks who begin their journey on a computer or smartphone are eventually required to use non-digital channels, such as printers and scanners. In some cases, they are even redirected to an in-person branch.

This is understandably infuriating for customers who sought to complete their account opening remotely and digitally. But customers that fail to onboard due to a broken digital process also represent lost opportunities for banks.

Consider that the average banking customer lifetime value is $45,600 (for the average customer lifespan of eight years).

Furthermore, Deloitte research shows that 40% of customers who begin opening an account at a bank never complete the process, mostly due to excess paperwork.

These lost opportunities really start to add up.

Practically by definition, digital-only banks bypass all these issues. Customers can’t be bounced to a physical branch because they don’t exist, and physical paperwork is similarly nonexistent.

As a result, Lightico’s study found that a mere 8% of customers who opened a new account with a digital-only bank between February and June 2020 said they experienced difficulty. This put digital-only banks in first place for ease of online account opening.

In contrast, the average account opening difficulty was 28% across all studied banks. In a few cases, the proportion of customers who experienced excess friction hovered around the 50% mark.

But this digital onboarding gap isn’t an inevitability. Traditional banks can emulate neobanks by revisiting their customers’ digital onboarding journey and recognize when outdated and cumbersome channels are causing needless friction — and introduce a digital alternative.

Much like a marriage that requires attention and care long after the vows have been exchanged, banks should continue to woo their existing customers through excellent servicing.

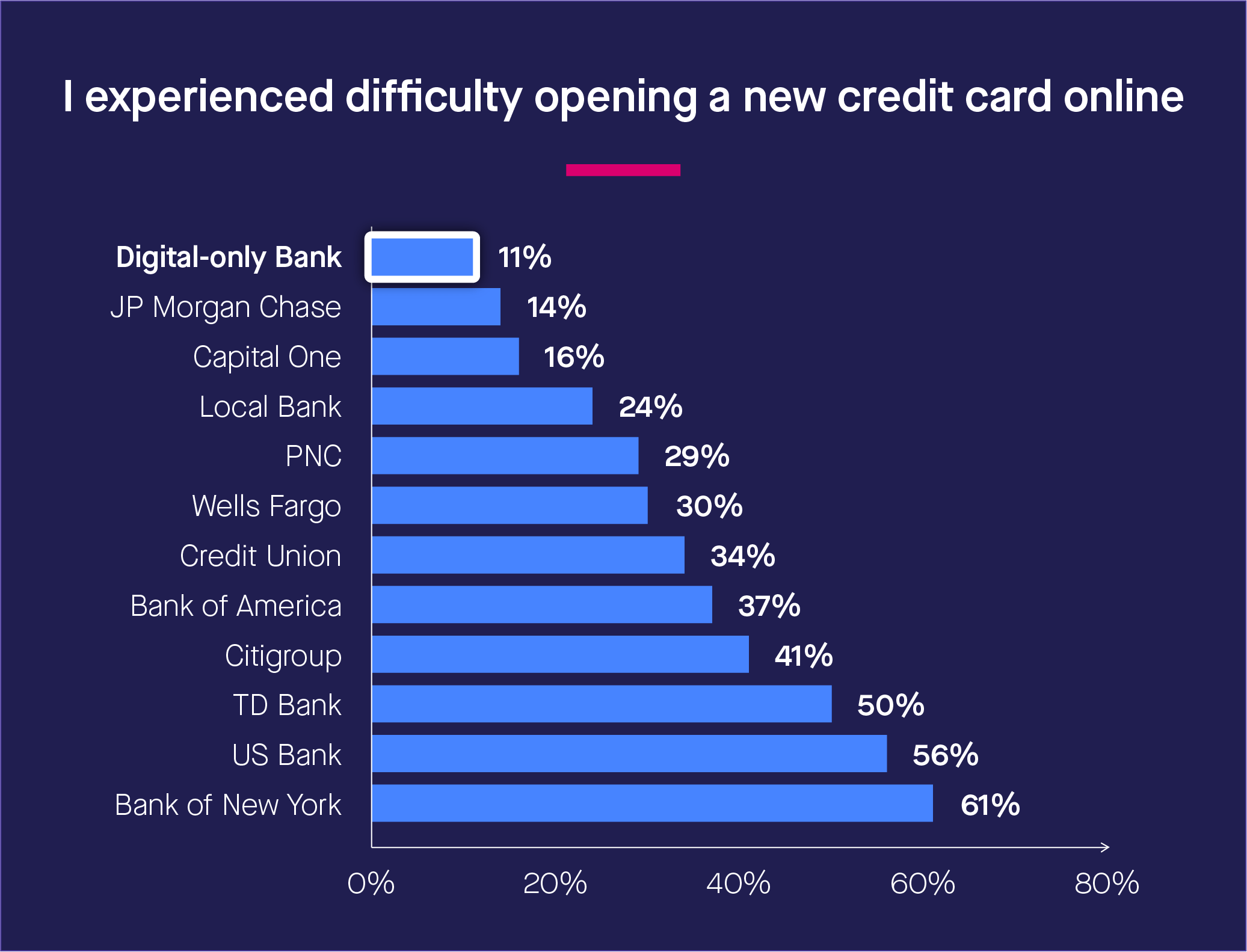

Unfortunately, here is another area that far too many banks needlessly botch. During the survey period, 34% of customers across a sample of 12 major banks and types of banks experienced difficulties when applying for a new credit card online. Troublingly, at some banks, a majority of customers found it difficult to apply for a credit card online.

During any time this would be unacceptable; after all, applying for a credit card is a routine activity that should be simple to undertake from any channel. During the pandemic, however, customers depended on smooth remote journeys in lieu of in-person servicing.

Here too, digital-only banks offered the easiest credit card opening process, with a mere 11% of digital-only customers experiencing difficulties. With physical paperwork and in-branch banking out of the equation by design, digital-only banks boast effortless credit card applications.

In contrast, traditional banks frequently include non-digital elements (e.g., mandatory branch visits, snail mail) in the digital credit card application process, perhaps out of habit.

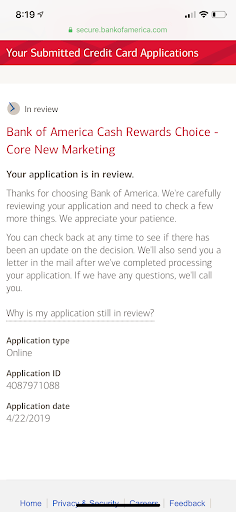

Below is a real-life example from a banking customer who tried to sign up for a credit card online with Bank of America. This customer now has to remember to check back the site regularly or wait for a letter to arrive in the mail to see her status.

A truly digital-first bank, not just a neobank, would simply send her a text message or email when her application was approved or denied. There is no reason for traditional banks to not do the same.

3. Satisfaction with service

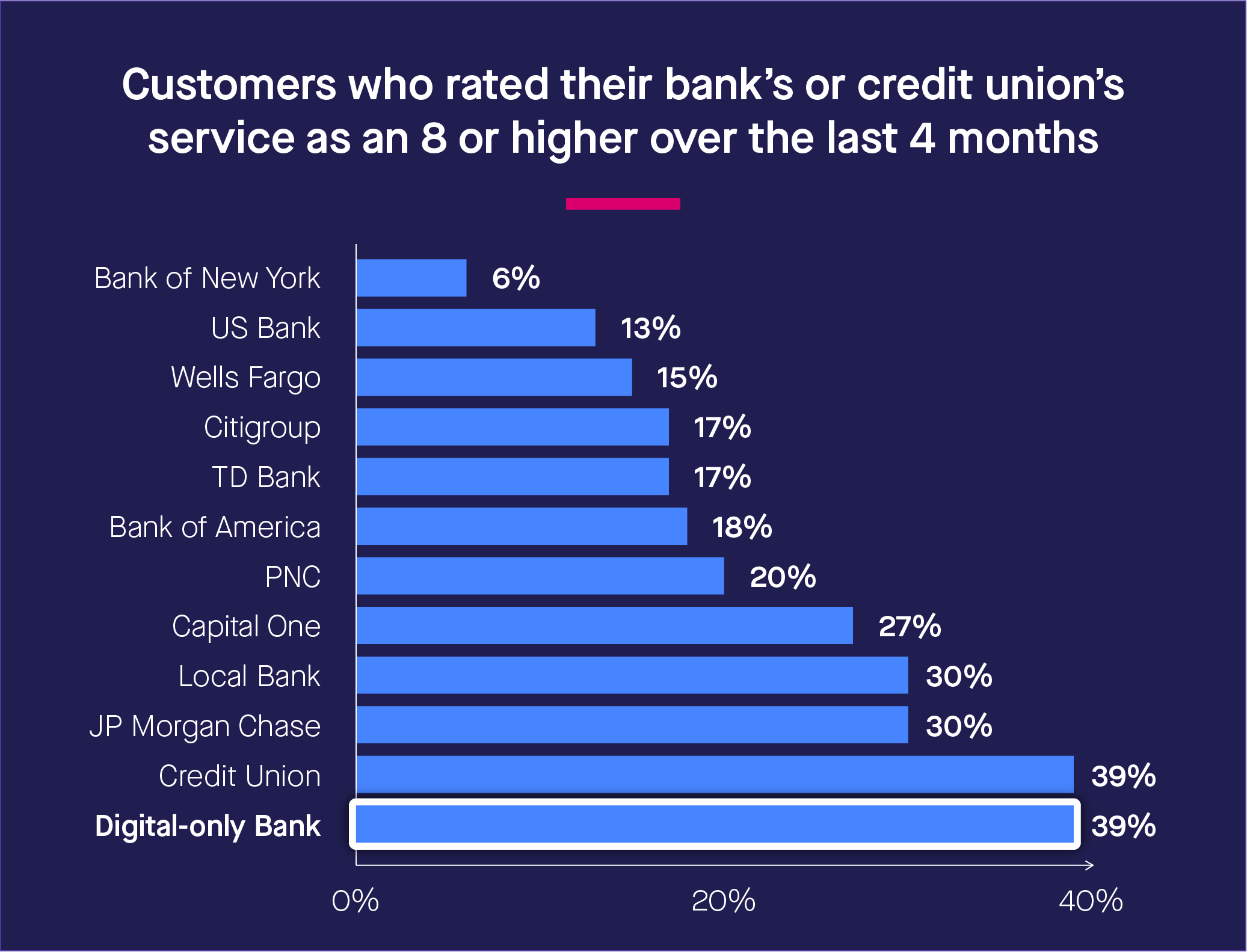

Customers of digital-only banks reported the highest levels of overall satisfaction with services; 39% rated their bank’s performance in the last four months an eight out of ten or higher.

In contradistinction, the digital laggards also come up as laggards overall. There is certainly impetus for digitization.

These findings demonstrate that digitization can’t be viewed as something separate from core banking activities. Banks that win at digital are rewarded with more satisfied customers. While correlation doesn’t always mean causation, it certainly suggests a meaningful pattern. With more and more customers heading online to complete banking tasks, it’s safe to assume that the ease of digital journeys has a powerful impact on overall satisfaction.

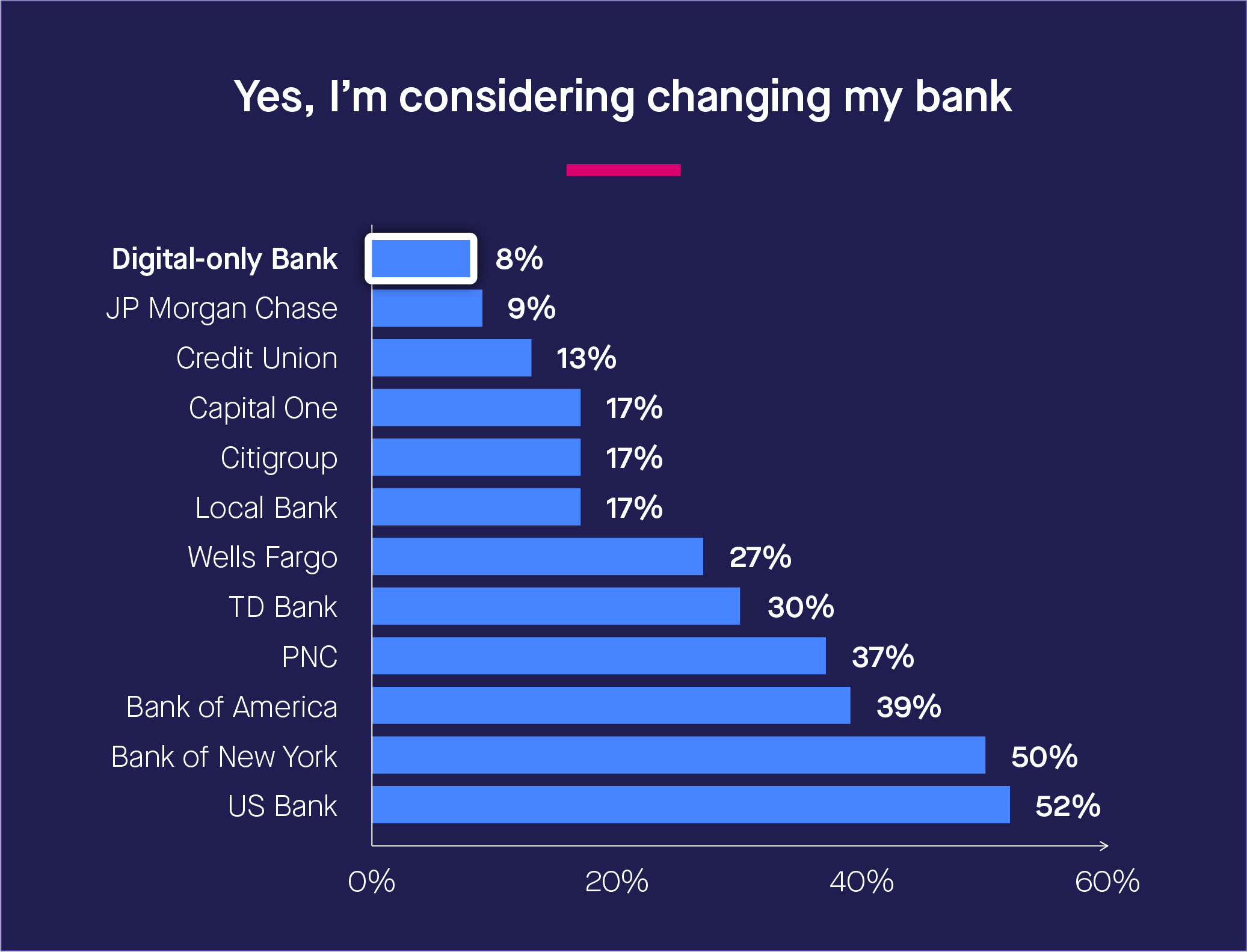

4. Loyalty and willingness to switch banks

When we think of engendering customer loyalty, what often comes to mind are images of high-quality in-person interactions between agents and consumers. While in-branch banking still has a role to play, this survey shows that loyalty can be built digitally and remotely.

A mere 8% of digital-only bank customers are considering switching banks, an average of 27% of customers across all banks. Notice that customers of banks that received the lowest marks for ease of digital account opening and credit card opening are the most likely to consider changing banks.

In other words, banks that offer seamless digital experiences are rewarded with greater loyalty, with digital-only banks leading the pack. Banks with difficult online processes take a dramatic loyalty hit.

Digital-first banks are exceeding customer expectations

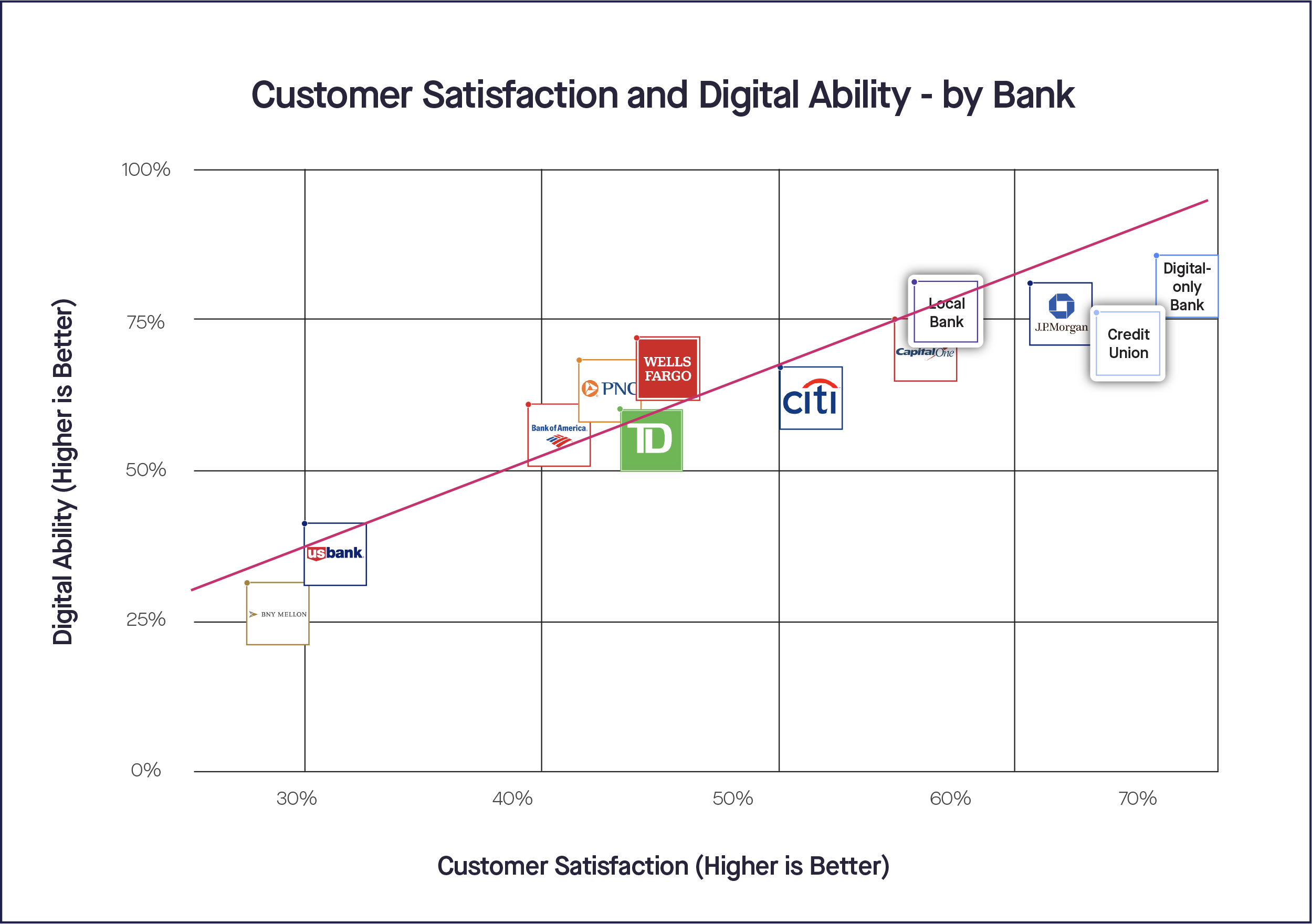

The survey findings enabled us to generate a quadrant graph demonstrating how banks measure up in two areas: customer experiencesatisfaction and digital ability.

Customer experience satisfaction was calculated by averaging customers’ ratings of their bank over the past four months and willingness to change banks right now (a signifier of loyalty).

Digital ability was calculated by averaging online interactions that had to be completed at a physical branch or required printing/scanning/faxing/e-mail to complete the journey. It also took into account the difficulty of opening a new account, taking or servicing a loan, and opening a new credit card online during the past four months.

When mapped out, a strong correlation emerges between banks’ CX and digital ability. The chart clearly shows that banks with favorable digital ratings tend to offer a superior overall CX.

Takeaway: Even banks that aren’t digital-only can be digital-first

To win over customers, financial institutions are recommended to take a leaf out of digital-only banks’ books. In fact, the traditional banks that came closest to providing a similar level of digital service as digital-only banks also received high marks for overall CX.

While not all banks should be digital-only, traditional banks can reap the rewards by mimicking the digital-only banks’ digital journeys — while continuing to provide in-person services as an alternative, not as a requirement.

By fixing broken digital journeys and bringing mobile-optimized eSignatures, eForms, and KYC procedures into the fray, banks will be better equipped to stay competitive with challenger banks while continuing to provide the broad array of services and resources traditional banks are known for.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

When customers attempt to open a bank account online, they intend to start and finish that process online. Unfortunately far too many customers of traditional banks who begin their journey on a computer or smartphone are eventually required to use non-digital channels, such as printers and scanners. In some cases, they are even redirected to an in-person branch.

This is understandably infuriating for customers who sought to complete their account opening remotely and digitally. But customers that fail to onboard due to a broken digital process also represent lost opportunities for banks.

Consider that the average banking customer lifetime value is $45,600 (for the average customer lifespan of eight years).

Furthermore, Deloitte research shows that 40% of customers who begin opening an account at a bank never complete the process, mostly due to excess paperwork.

These lost opportunities really start to add up.

Practically by definition, digital-only banks bypass all these issues. Customers can’t be bounced to a physical branch because they don’t exist, and physical paperwork is similarly nonexistent.

As a result, Lightico’s study found that a mere 8% of customers who opened a new account with a digital-only bank between February and June 2020 said they experienced difficulty. This put digital-only banks in first place for ease of online account opening.

In contrast, the average account opening difficulty was 28% across all studied banks. In a few cases, the proportion of customers who experienced excess friction hovered around the 50% mark.

But this digital onboarding gap isn’t an inevitability. Traditional banks can emulate neobanks by revisiting their customers’ digital onboarding journey and recognize when outdated and cumbersome channels are causing needless friction — and introduce a digital alternative.

When customers attempt to open a bank account online, they intend to start and finish that process online. Unfortunately far too many customers of traditional banks who begin their journey on a computer or smartphone are eventually required to use non-digital channels, such as printers and scanners. In some cases, they are even redirected to an in-person branch.

This is understandably infuriating for customers who sought to complete their account opening remotely and digitally. But customers that fail to onboard due to a broken digital process also represent lost opportunities for banks.

Consider that the average banking customer lifetime value is $45,600 (for the average customer lifespan of eight years).

Furthermore, Deloitte research shows that 40% of customers who begin opening an account at a bank never complete the process, mostly due to excess paperwork.

These lost opportunities really start to add up.

Practically by definition, digital-only banks bypass all these issues. Customers can’t be bounced to a physical branch because they don’t exist, and physical paperwork is similarly nonexistent.

As a result, Lightico’s study found that a mere 8% of customers who opened a new account with a digital-only bank between February and June 2020 said they experienced difficulty. This put digital-only banks in first place for ease of online account opening.

In contrast, the average account opening difficulty was 28% across all studied banks. In a few cases, the proportion of customers who experienced excess friction hovered around the 50% mark.

But this digital onboarding gap isn’t an inevitability. Traditional banks can emulate neobanks by revisiting their customers’ digital onboarding journey and recognize when outdated and cumbersome channels are causing needless friction — and introduce a digital alternative.

Much like a marriage that requires attention and care long after the vows have been exchanged, banks should continue to woo their existing customers through excellent servicing.

Unfortunately, here is another area that far too many banks needlessly botch. During the survey period, 34% of customers across a sample of 12 major banks and types of banks experienced difficulties when applying for a new credit card online. Troublingly, at some banks, a majority of customers found it difficult to apply for a credit card online.

During any time this would be unacceptable; after all, applying for a credit card is a routine activity that should be simple to undertake from any channel. During the pandemic, however, customers depended on smooth remote journeys in lieu of in-person servicing.

Here too, digital-only banks offered the easiest credit card opening process, with a mere 11% of digital-only customers experiencing difficulties. With physical paperwork and in-branch banking out of the equation by design, digital-only banks boast effortless credit card applications.

In contrast, traditional banks frequently include non-digital elements (e.g., mandatory branch visits, snail mail) in the digital credit card application process, perhaps out of habit.

Below is a real-life example from a banking customer who tried to sign up for a credit card online with Bank of America. This customer now has to remember to check back the site regularly or wait for a letter to arrive in the mail to see her status.

A truly digital-first bank, not just a neobank, would simply send her a text message or email when her application was approved or denied. There is no reason for traditional banks to not do the same.

Much like a marriage that requires attention and care long after the vows have been exchanged, banks should continue to woo their existing customers through excellent servicing.

Unfortunately, here is another area that far too many banks needlessly botch. During the survey period, 34% of customers across a sample of 12 major banks and types of banks experienced difficulties when applying for a new credit card online. Troublingly, at some banks, a majority of customers found it difficult to apply for a credit card online.

During any time this would be unacceptable; after all, applying for a credit card is a routine activity that should be simple to undertake from any channel. During the pandemic, however, customers depended on smooth remote journeys in lieu of in-person servicing.

Here too, digital-only banks offered the easiest credit card opening process, with a mere 11% of digital-only customers experiencing difficulties. With physical paperwork and in-branch banking out of the equation by design, digital-only banks boast effortless credit card applications.

In contrast, traditional banks frequently include non-digital elements (e.g., mandatory branch visits, snail mail) in the digital credit card application process, perhaps out of habit.

Below is a real-life example from a banking customer who tried to sign up for a credit card online with Bank of America. This customer now has to remember to check back the site regularly or wait for a letter to arrive in the mail to see her status.

A truly digital-first bank, not just a neobank, would simply send her a text message or email when her application was approved or denied. There is no reason for traditional banks to not do the same.

Customers of digital-only banks reported the highest levels of overall satisfaction with services; 39% rated their bank’s performance in the last four months an eight out of ten or higher.

In contradistinction, the digital laggards also come up as laggards overall. There is certainly impetus for digitization.

These findings demonstrate that digitization can’t be viewed as something separate from core banking activities. Banks that win at digital are rewarded with more satisfied customers. While correlation doesn’t always mean causation, it certainly suggests a meaningful pattern. With more and more customers heading online to complete banking tasks, it’s safe to assume that the ease of digital journeys has a powerful impact on overall satisfaction.

Customers of digital-only banks reported the highest levels of overall satisfaction with services; 39% rated their bank’s performance in the last four months an eight out of ten or higher.

In contradistinction, the digital laggards also come up as laggards overall. There is certainly impetus for digitization.

These findings demonstrate that digitization can’t be viewed as something separate from core banking activities. Banks that win at digital are rewarded with more satisfied customers. While correlation doesn’t always mean causation, it certainly suggests a meaningful pattern. With more and more customers heading online to complete banking tasks, it’s safe to assume that the ease of digital journeys has a powerful impact on overall satisfaction.

When we think of engendering customer loyalty, what often comes to mind are images of high-quality in-person interactions between agents and consumers. While in-branch banking still has a role to play, this survey shows that loyalty can be built digitally and remotely.

A mere 8% of digital-only bank customers are considering switching banks, an average of 27% of customers across all banks. Notice that customers of banks that received the lowest marks for ease of digital account opening and credit card opening are the most likely to consider changing banks.

In other words, banks that offer seamless digital experiences are rewarded with greater loyalty, with digital-only banks leading the pack. Banks with difficult online processes take a dramatic loyalty hit.

When we think of engendering customer loyalty, what often comes to mind are images of high-quality in-person interactions between agents and consumers. While in-branch banking still has a role to play, this survey shows that loyalty can be built digitally and remotely.

A mere 8% of digital-only bank customers are considering switching banks, an average of 27% of customers across all banks. Notice that customers of banks that received the lowest marks for ease of digital account opening and credit card opening are the most likely to consider changing banks.

In other words, banks that offer seamless digital experiences are rewarded with greater loyalty, with digital-only banks leading the pack. Banks with difficult online processes take a dramatic loyalty hit.

The survey findings enabled us to generate a quadrant graph demonstrating how banks measure up in two areas: customer experience satisfaction and digital ability.

Customer experience satisfaction was calculated by averaging customers’ ratings of their bank over the past four months and willingness to change banks right now (a signifier of loyalty).

Digital ability was calculated by averaging online interactions that had to be completed at a physical branch or required printing/scanning/faxing/e-mail to complete the journey. It also took into account the difficulty of opening a new account, taking or servicing a loan, and opening a new credit card online during the past four months.

When mapped out, a strong correlation emerges between banks’ CX and digital ability. The chart clearly shows that banks with favorable digital ratings tend to offer a superior overall CX.

The survey findings enabled us to generate a quadrant graph demonstrating how banks measure up in two areas: customer experience satisfaction and digital ability.

Customer experience satisfaction was calculated by averaging customers’ ratings of their bank over the past four months and willingness to change banks right now (a signifier of loyalty).

Digital ability was calculated by averaging online interactions that had to be completed at a physical branch or required printing/scanning/faxing/e-mail to complete the journey. It also took into account the difficulty of opening a new account, taking or servicing a loan, and opening a new credit card online during the past four months.

When mapped out, a strong correlation emerges between banks’ CX and digital ability. The chart clearly shows that banks with favorable digital ratings tend to offer a superior overall CX.