How Can Banks Support Troops Abroad & Ensure SCRA Compliance?

By David Abbou

While the volume of Servicemembers Civil Relief Act (SCRA) cases is generally very low, managing this heavily regulated process is especially critical for banks given the steep penalties banks can face for noncompliance.

But processing of SCRA requests to date has been filled with friction and frustration — banks and financial institutions today need a swift and efficient way to manage these processes while ensuring compliance.

In this blog, we’ll explain:

The purpose of SCRA, eligibility for benefits, and what these benefits include for banking customers

The pain of current SCRA banking processes for both banks and their customers

What banks need to quickly and efficiently complete SCRA processes and ensure compliance

What is the purpose of the SCRA?

The Servicemembers Civil Relief Act (SCRA) was first enacted in 2003 to support U.S. citizens enlisted in the military and their families in coping with financial challenges they face during active duty.

The spirit of this law is to help American servicemembers focus their energies on the defense of the nation.

What are the challenges faced by military personnel & their families?

Commissioned members of the Public Health Service and the National Oceanographic and Atmospheric Administration may also be eligible for these benefits.

In 2021, over 1.4 million U.S. citizens are active members of the armed forces. Approximately 165,000 of the military’s active-duty personnel are stationed outside the United States and its territories.

The mobile military life brings with it challenges for many American families. At 24%, unemployment rates for military spouses were far higher than the general population in 2020.

Which banking customers are eligible for SCRA benefits?

Any member and reservist on active duty in the U.S. military, including the Army, Navy, Air Force, Marine Corps, National Guard, and Coast Guard is eligible to receive SCRA benefits.

Military spouses are also entitled to certain SCRA protections, as covered in the second amendment to the SCRA called the Veterans Benefits and Transition Act of 2018.

When must banks provide SCRA benefits to eligible banking customers?

Any eligible banking customer is legally entitled to receive SCRA benefits on the date they enter active duty. Under the legislation, eligible citizens are to receive full SCRA benefits for the entire time they are on active duty.

This coverage typically terminates within 30 to 90 days after the end or discharge from active duty.

What do SCRA benefits include?

There are numerous benefits that banks and financial institutions must provide to SCRA-eligible customers. Some of the main benefits are:

A cap on interest rates: Interest rates for any U.S. bank mortgage, loan, line of credit, or credit card opened prior to the customer being called to active duty is capped at 6%. Also, banking fees must be waived for these accounts while the banking customer is on active military service.

Enforced limits on foreclosures: SCRA members experiencing difficulty in paying mortgages are protected from foreclosure on their home by the bank. This is a specifically tricky aspect of SCRA legislation for banks as the law does not clearly stipulate if the customer has to advise the bank when they begin active duty — putting the onus on banks to determine the borrower’s military status. Any bank or financial institution must obtain a court order to move forward with a foreclosure on a service member — proceeding with a foreclosure can result in severe fines for banks found to be in non-compliance of the SCRA laws.

Protection against repossession of a vehicle: Similar to foreclosures, any bank or auto lender repossessing a vehicle of an SCRA member without first obtaining a court order can face hefty fines.

How long do SCRA benefits last?

For home loans, members protected by the SCRA receive an interest rate reduction for 12 months after completing their military service. Interest rate reductions and other benefits for all other installment loans expire 6 months after the member is discharged from active duty.

How can banks protect themselves against fraudulent SCRA claims?

Of course, like with many other benefits, abuses can and do occur. Banks can verify whether a customer is actively in the military or not by doing a check on their social security on the Defense Manpower Data Center website.

Broken SCRA Processes: Painful for Customers, Risky for Banks

As mentioned, the amount of legal scrutiny and regulation by the U.S. Department of Justice makes it especially vital for banks and financial institutions to have an efficient and compliant SCRA process.

A banking customer that’s actively on military duty needs the quickest process possible to report their SCRA status and apply for benefits — and this is often uniquely challenging since many servicemen and women are stationed overseas for prolonged periods of time.

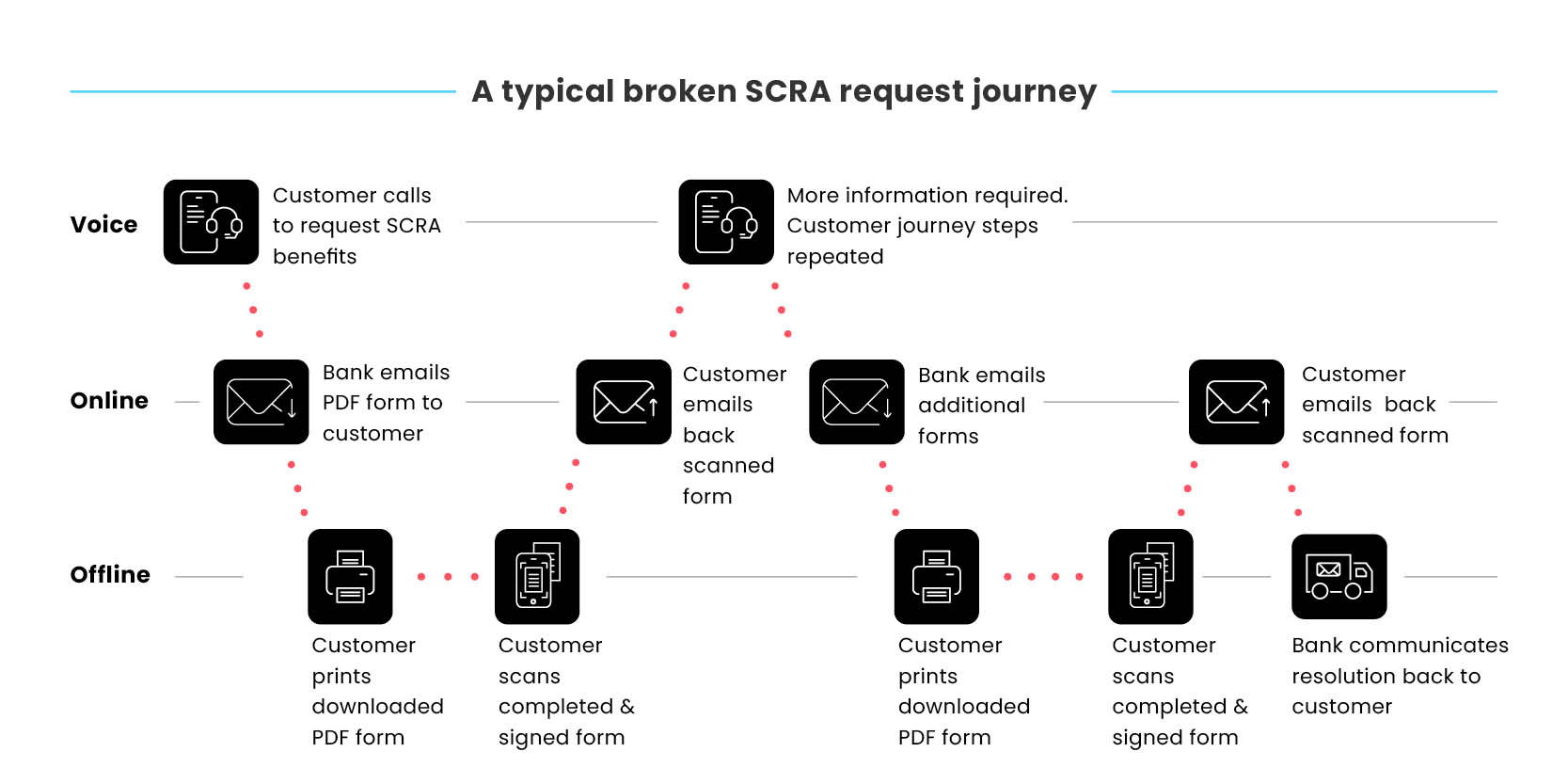

What does this process usually look like for a serviceman or woman serving abroad?

This customer may look for an online benefits request form to report their SCRA status to their bank or simply call a toll-free number and speak to a contact center agent. But to process the request, their bank will typically require additional supporting documents from the customer, including:

The servicemember’s name

Social Security Number

Active duty start date

Branch of service

But when you look at most banking processes to handle SCRA processes today, few have evolved significantly since the 1990s.

To acquire these documents, the bank will email the customer a PDF form to fill out and sign. Crowded PDF forms make for an uncomfortable experience for banking customers in general., especially on mobile. In fact, most will wait until they arrive home and download that PDF form using their desktop or laptop. A customer on-duty may not have that option.

The next step is just as difficult, as the customer will need to print, fill out the form, and get it back to the bank. Bouncing from phone call, to email, to printing and sending back a PDF form is frustrating and inconvenient to any customer.

But asking a customer stationed overseas to find old school tech like a printer, fax machine or scanner? Sounds like a particularly uncomfortable mission. They may turn to plain old snail mail, if only they can find a mailbox nearby…

What can and does happen frequently, is that this customer will simply throw up their hands and push off dealing with the SCRA process altogether.

For banks and financial institutions these broken journeys add complexity and friction for customers who are already dealing with enough stress during their military service.

Worse yet, an incomplete SCRA process can be a damaging and costly blind spot for banks, since customers don’t explicitly have to report to their bank when they start active duty.

Banks without a process that verifies the customers’ SCRA status can mistakenly attempt to get a default judgment to foreclose on property or enforce a loan when the customer is actually protected by the SCRA, putting them in violation of the law.

Not having a thorough process that covers all of the requirements needed both from the bank and customer can lead to costly fines and damaging press coverage that can have lasting negative impact on a bank’s brand.

Situations like this arise due to banks’ dependence on digital silos and legacy processes.

Digital Silos and Legacy Processes Are Sending SCRA Customers on an Unnecessary Mission

In their attempts to automate workflows, banks have implemented multiple point solutions to help complete each step of the customer’s journey, such as ID verification, digital signatures and eForms, and document collection.

But none of these systems effectively talk to one another, and it’s because they operate in silos that customer-facing processes demand multiple steps, needlessly prolonging the journey for the customer.

Legacy processes, like PDF-based forms, and those printers and fax machines we mentioned earlier, add work and hassle for customers just so they can simply request and confirm their SCRA benefits. That includes driving a customer to the app store to install an e-signature app just to sign an SCRA benefits request form, as the process hardly stops there and they’re likely to have questions about what’s required of them, forcing them to make another call to the contact center or branch.

Digitally Completing the Entire SCRA Request

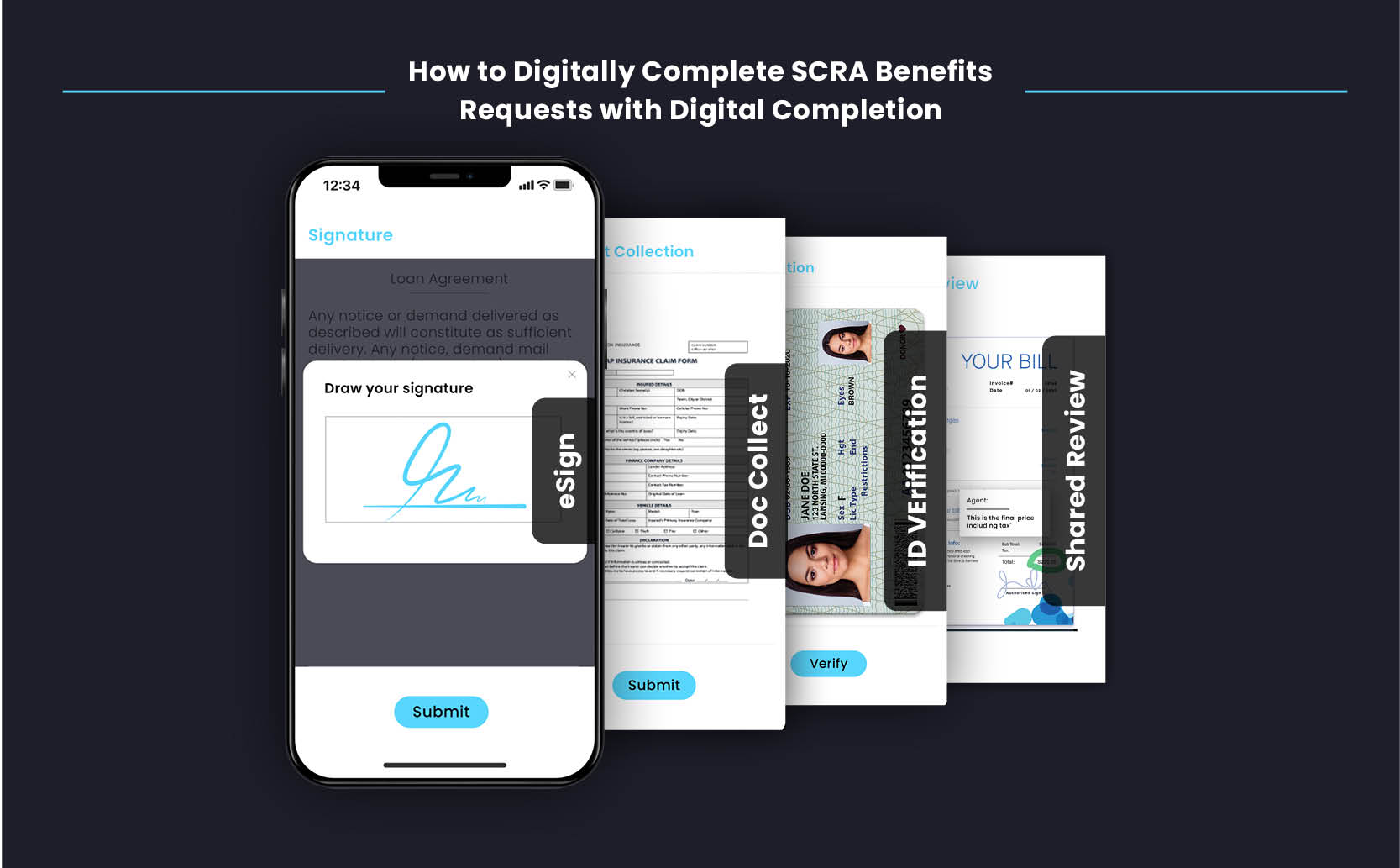

To rid themselves of these broken journeys, banks require an end-to-end digital solution that gives customers one seamless digital experience and quickly and transparently guides them through the entire SCRA benefits process, right on to completion.

Digital Completion technology has evolved today that allows banks to consolidate all customer-facing tasks into a single interactive experience, including eForms, eSignature, ID verification, document collection, and more.

Instead of downloading and filling out multiple forms, banking customers today can open a link received by SMS or email, and tap and swipe through each step in one simple and user-friendly digital session.

Banks currently delivering digitally complete journey for SCRA requests are seeing improved:

Customer access

First-call Resolution

Turnaround Times for document collection

NPS / CSAT

Customer experience

Compliance

Digitally completing these steps for troops and their families not only saves them time and effort, it prevents unnecessary headaches and gives them peace of mind — this strengthens customer loyalty for banks while improving compliance.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

For banks and financial institutions these broken journeys add complexity and friction for customers who are already dealing with enough stress during their military service.

Worse yet, an incomplete SCRA process can be a damaging and costly blind spot for banks, since customers don’t explicitly have to report to their bank when they start active duty.

Banks without a process that verifies the customers’ SCRA status can mistakenly attempt to get a default judgment to foreclose on property or enforce a loan when the customer is actually protected by the SCRA, putting them in violation of the law.

Not having a thorough process that covers all of the requirements needed both from the bank and customer can lead to costly fines and damaging press coverage that can have lasting negative impact on a bank’s brand.

Situations like this arise due to banks’ dependence on digital silos and legacy processes.

For banks and financial institutions these broken journeys add complexity and friction for customers who are already dealing with enough stress during their military service.

Worse yet, an incomplete SCRA process can be a damaging and costly blind spot for banks, since customers don’t explicitly have to report to their bank when they start active duty.

Banks without a process that verifies the customers’ SCRA status can mistakenly attempt to get a default judgment to foreclose on property or enforce a loan when the customer is actually protected by the SCRA, putting them in violation of the law.

Not having a thorough process that covers all of the requirements needed both from the bank and customer can lead to costly fines and damaging press coverage that can have lasting negative impact on a bank’s brand.

Situations like this arise due to banks’ dependence on digital silos and legacy processes.

Banks currently delivering digitally complete journey for SCRA requests are seeing improved:

Banks currently delivering digitally complete journey for SCRA requests are seeing improved: