Post-COVID-19 Survey: Consumers Want Digital Banking to Stay

By Leor Melamedov

There is plenty of talk in the banking community about getting back to normal business operations.

Most of the conversation at the executive level surrounds the process of reopening bank branches: when should they be fully reopened, what safety measures should be put in place.

The problem is that these discussions leave out the most important player in all of this: the customer. Do customers even want to go back to a reality where “business as usual” means long lines, bounded banking hours, and lots of paperwork?

The latest results from a series of surveys of American banking customers suggests the answer is a resounding “no.”

There is no need to speculate about what the future holds. The hard data show over and over that customers are expecting banks to expand their remote and digital offerings –– not just sanitize their branches. Consumers have wanted this for years, but this time, banks have to listen and act.

Before the coronavirus: Customers stumbled through choppy journeys

The coronavirus may have highlighted the need for more and better digital banking. But consumer demand for remote transactions –– and frustration with traditional processes –– was high long before safety concerns entered into the equation.

For example, a November 2019 survey found that 77% of low- and middle-income customers said a better mobile experience elsewhere would influence their decision to leave their original bank. To compare, 63% would be influenced by lower fees, and a paltry 28% would make the switch for more branches or ATMs.

This shouldn’t come as a surprise. Broken digital journeys are incredibly frustrating. Customers who begin their journey on an online channel expect to finish the process online, but they are frequently redirected to other channels or a physical branch.

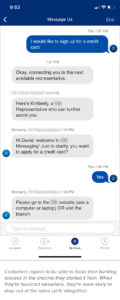

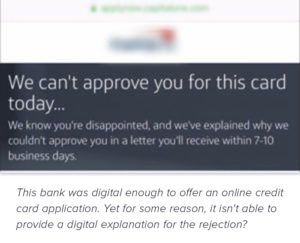

Here are just a few actual instances we captured of digital banking gone wrong:

Unfortunately, broken digital journeys such as these were far from the exception. But while large players were making slow, incomplete changes due to compliance fears and sheer inertia, neobanks waited in the wings to bring fed-up customers into the fold.

During the coronavirus: banks’ great digital leap forward

Then, the coronavirus hit. As the infectious disease swept the globe, banks, like all businesses, were shaken out of their complacency.

One thing became clear: Protecting customers and bank employees would necessitate moving to fully remote transactions.

For example, getting PPP funds into small business’ bank accounts quickly required the adoption of automation and doing away with manual data entry. Banks such as Texas-based Happy State Bank mobilized quickly and digitally to serve customers remotely under tight timeframes.

Many banks began adopting and promoting digital transaction capabilities such as eSignatures, remote document collection, chat bots, and text messaging-based customer communication.

Initiatives that would’ve taken years for slow-moving banks to implement were put into place in a matter of weeks. It took a major crisis, complete with branch closures and soft closures, to force these much-needed changes. But banks rose to the occasion, successfully transitioning to remote processes.

Our research confirms that banks’ prioritization of digital services was the correct response.

Early on in the pandemic (March 15, 2020), we surveyed more than 1,000 consumers on the impact of COVID-19 on their daily lives and preferences.

Even at that relatively early stage of the crisis, over half of customers expressed financial concerns, which in some cases led to interest in deferments, refinancing, or extra cash via a loan. Yet 49% said they would be less likely to take out a bank loan if it required going to a physical branch. The takeaway was clear: banking customers need access to financial services, perhaps more than ever during the coronavirus. But many customers would avoid such important services if remote options weren’t available.

Now and after the coronavirus: digital as default?

Now that we’re potentially starting to slowly emerge from the pandemic, banking executives are wondering –– what’s next? To answer that, it helps to remember how demand for digital services was already very high before the coronavirus hit. Pre-coronavirus, 77% of low- to middle-income customers would choose a new bank based on how digital-friendly it was. Let that number sink in for a second.

Banks who promoted fully remote services during the coronavirus crisis should first and foremost pay attention to what customers want going forward –– and we saw that this is a continuation of the digital servicing they received at the height of the crisis.

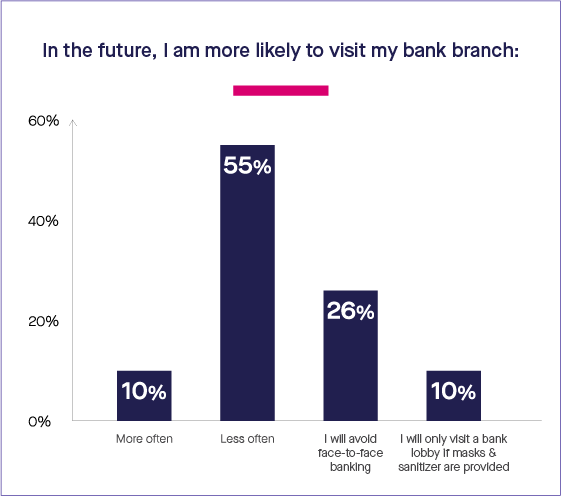

Our most recent survey of 1,028 Americans conducted in mid-May 2020 found that consumers continue to express a growing desire for digital, remote options. And consistent with previous findings, they are willing to skip visits if it means visiting a physical branch. In fact:

55% of consumers say they plan to visit branches less often in the future.

26% say they will avoid face-to-face banking altogether.

Just 10% say they would only visit a branch if masks and hand sanitizers are available there.

The takeaway here is that while it’s certainly important to implement safety measures when reopening branches, banking executives who focus on this are missing the greater point. The majority of consumers now want to conduct the majority of their banking online.

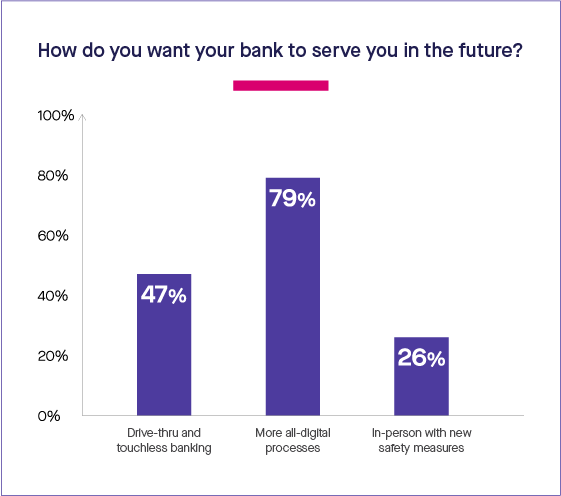

In-person banking still has a role to play, especially when it comes to highly complex issues. But it’s no longer seen as the ideal for the vast majority of transactions. A whopping 79% of customers now say that they want more all-digital processes from their bank in the future. Another 47% look forward to drive-thru or touchless banking. In contrast, a mere 26% would prefer in-person banking with safety measures.

The post-coronavirus new normal: all digital

Customers have spoken, and the results are in: they don’t see digital and remote services as a temporary, makeshift solution. On the contrary, they want digital banking to be the default way of banking, with in-person transactions reserved for sensitive matters where advice is needed, not transactions.

Bankers are busy discussing a return to the “new normal,” with the implication that going back to the usual way of doing things (i.e., in-person, paperwork-heavy transactions) is desirable. But the evidence shows that in-person is not as core as we once thought. In fact, people will actually pass on financial transactions if they are cumbersome and branch-based. Customers have tasted the convenience and ease of remote banking –– and they like it.

Primary banks should think very carefully about going back to relying on in-person processes. Those that do should know it’s just a matter of time before customers take their business to a digital-first competitor that learned the right lessons from the crisis.

Read the whole story here.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Unfortunately, broken digital journeys such as these were far from the exception. But while large players were making slow, incomplete changes due to compliance fears and sheer inertia, neobanks waited in the wings to bring fed-up customers into the fold.

Unfortunately, broken digital journeys such as these were far from the exception. But while large players were making slow, incomplete changes due to compliance fears and sheer inertia, neobanks waited in the wings to bring fed-up customers into the fold.

The takeaway here is that while it’s certainly important to implement safety measures when reopening branches, banking executives who focus on this are missing the greater point. The majority of consumers now want to conduct the majority of their banking online.

In-person banking still has a role to play, especially when it comes to highly complex issues. But it’s no longer seen as the ideal for the vast majority of transactions. A whopping 79% of customers now say that they want more all-digital processes from their bank in the future. Another 47% look forward to drive-thru or touchless banking. In contrast, a mere 26% would prefer in-person banking with safety measures.

The takeaway here is that while it’s certainly important to implement safety measures when reopening branches, banking executives who focus on this are missing the greater point. The majority of consumers now want to conduct the majority of their banking online.

In-person banking still has a role to play, especially when it comes to highly complex issues. But it’s no longer seen as the ideal for the vast majority of transactions. A whopping 79% of customers now say that they want more all-digital processes from their bank in the future. Another 47% look forward to drive-thru or touchless banking. In contrast, a mere 26% would prefer in-person banking with safety measures.