Regulatory Complaints Are Needlessly Painful: How Banks Can Prevent Them

By David Abbou

There are a wide variety of issues and disputes that can arise between banks and financial institutions and their customers. Efficiently resolving these banking disputes before they flare up is critical for banks to protect these customer relationships and their long-term loyalty.

But inevitably, there will be scenarios where a customer has escalated an unresolve issue up to the bank’s Office of the President or as high as they can take it from within — and if the process is full of friction and takes too long to resolve to their satisfaction they will often look to file a complaint with regulators or other agencies.

Why do so many of these issues escalate to this point, risk tying up banks in regulatory investigations, and often result in losing that customer for good?

Sadly for banks, many of these issues escalate to the point of no return not because the issue itself can't be resolved with their customer, but because steps to getting to that resolution are made so complex and painful that the customer’s frustration boils over, making them lose faith in them entirely.

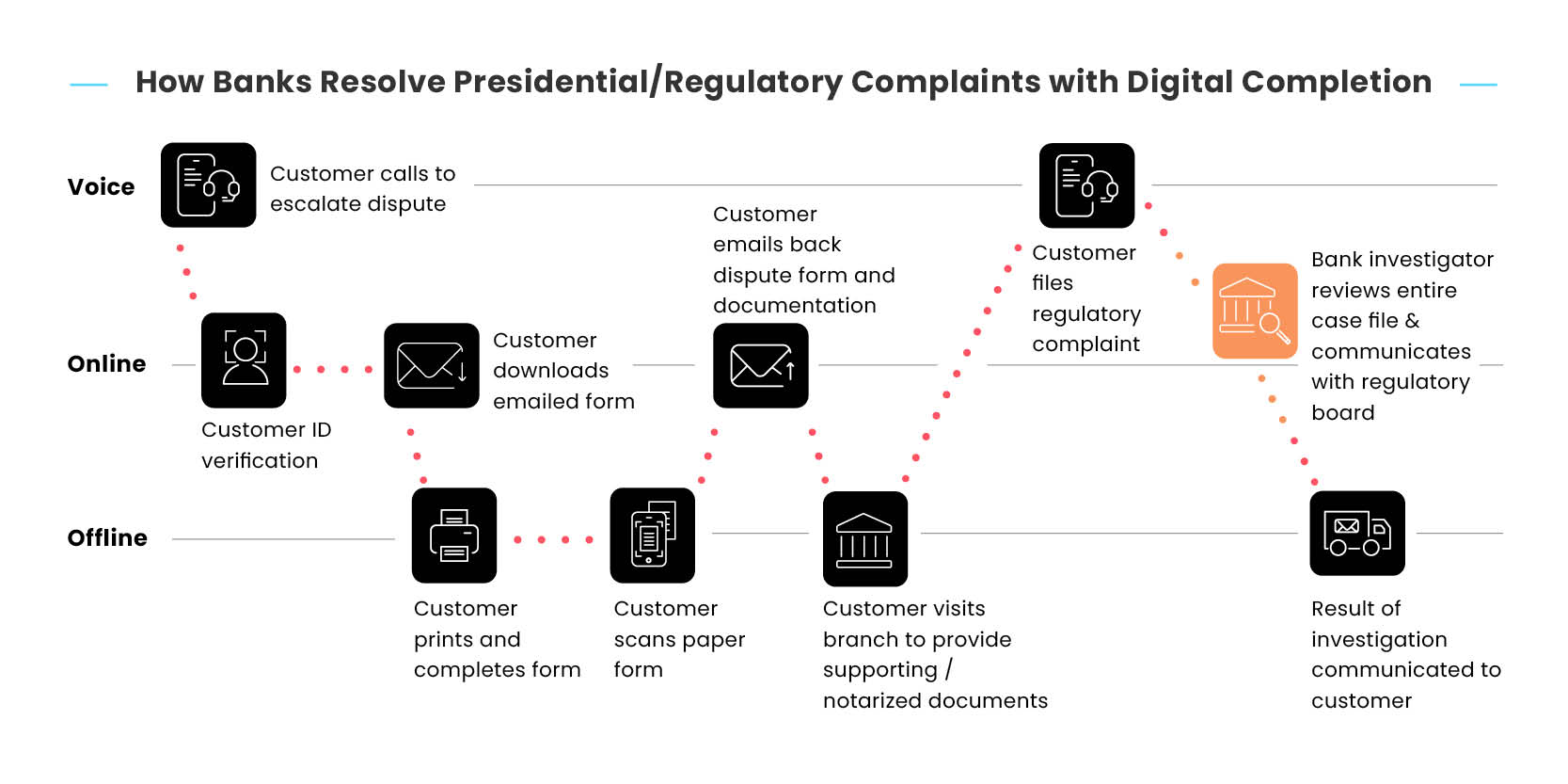

Think about what current advanced dispute workflows ask from banking customers. For example, take a customer who booked airline tickets using their bank-issued credit card, only the airline ended up needing to cancel the flight, and for some reason never ended up refunding the booking amount to the customer. Say this customer booked the flight through a booking engine using points from their credit card’s loyalty reward program.

Already, we have several parties and departments involved in this one dispute: The airline, the booking website, the credit card company’s loyalty rewards program, and of course the bank who's left responsible to investigate and resolve the matter.

Engaging with each of these parties, their processes and the inevitable paperwork that’s involved elongates the process for banks and many times leads to servicing and communication gaps that leave customers hanging — exacerbating what may already be a heated situation.

Having been made to spend hours on the phone and fill out multiple forms, the customer loses confidence that they’ll see their money refunded without further delay… their patience snaps, and they contact their state regulator or the Consumer Financial Protection Bureau (CFPB).

Here’s what the customer typically hears when chasing a resolution from all these parties:

Banks want to do better, but their current process just won’t let them: Locking financial institutions into these broken journeys is their dependence on digital silos and legacy processes.

Digital Silos & Legacy Processes Push Customer Patience Over the Edge

Banks have invested a great deal in digitizing their core systems with the aim of reducing paperwork and saving time for both them and their customers.

When it comes to their frontend customer-facing systems however, they’ve done their best to glue together a collection of point solutions — none of which integrate seamlessly with another and operate essentially as silos.

This means customers may first speak with an agent at the call center hoping they can guide them through the resolution process, only to be told they need to fill out complex dispute forms, add screenshots of payment confirmation, and depending on the nature of the dispute may need to visit their local branch.

In advanced banking disputes these steps can span multiple departments and even extend to regulatory investigations with external organizations, being able to integrate every step needed from the customer is crucial to minimizing the red tape and ultimately frustration between customer and bank.

Manual legacy processes pretty much ensure these experiences are even more painstaking. Imagine having a lengthy dispute with your bank and being asked to download an e-signature app from the app store for this one time.

Then, when you check your email and download that lengthy and clunky PDF form it becomes obviously clear, there’s no way you’re doing this digitally. You end up printing out that form and filling it out manually. Then, instead of heading home after your commute, you track down an Office Depot just so you can scan that form and send it back to the bank.

That’s why these outdated legacy channels are a part of the problem — not the solution — for banks needing to resolve regulatory complaints or any banking dispute process for that matter.

Banks Turning to Digital Completion to Speed Up Resolution of Regulatory Complaints

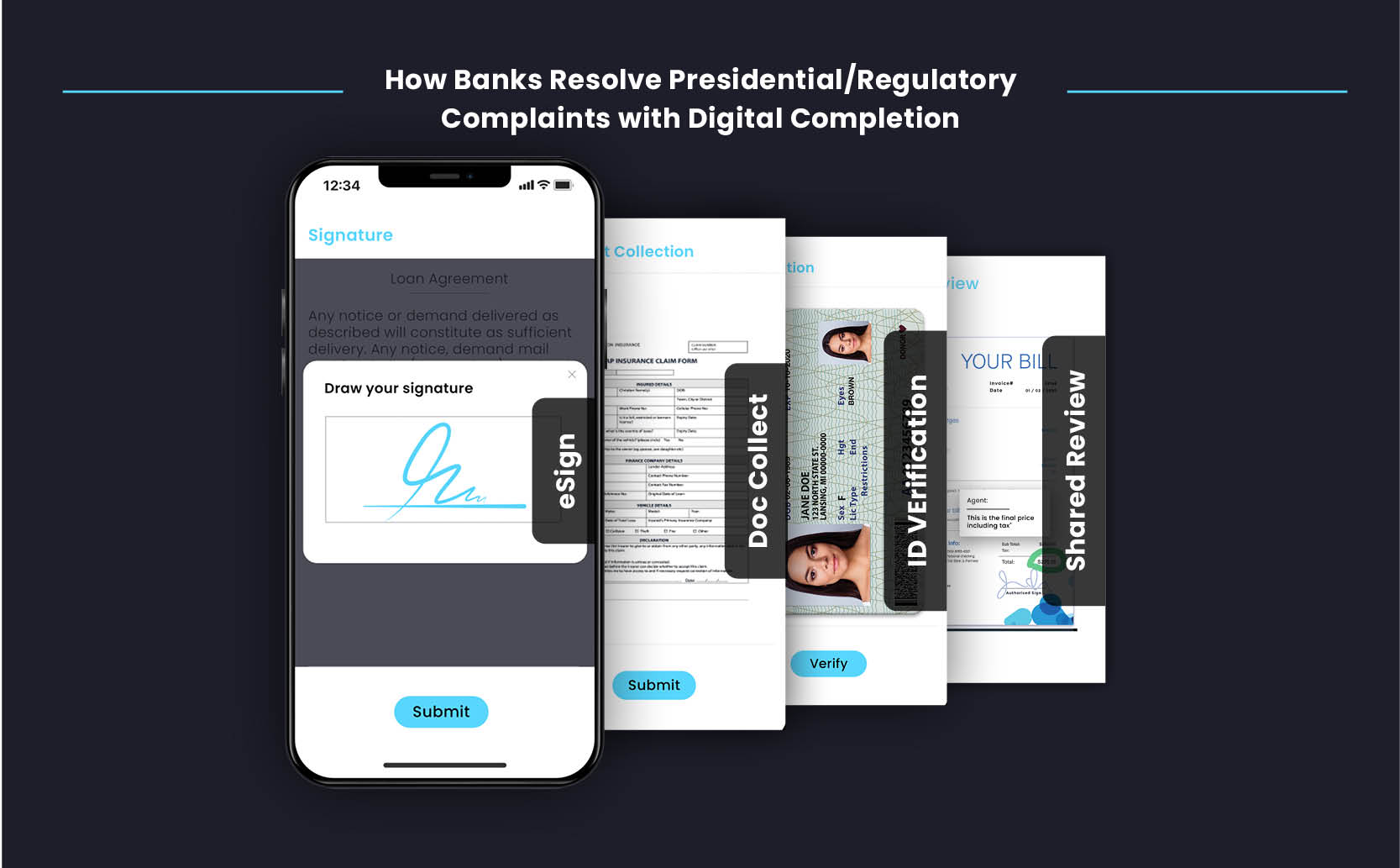

A Digital Completion platform can offer a solid audit trail for any and all documents collected and shared during presidential/regulatory complaints, as well as real-time messaging with an agent. This allows for a <st< span="">rong>formal and well-documented engagement process and provides an efficient way to communicate and review the complaint with customers.</st<>

Thanks to emerging technology, banks and financial institutions can digitize every step of the customer journey, including ID verification, completion of eForms, collecting documents, terms and conditions, and e-signatures for virtually every customer-facing process. Customers complete all steps by simply tapping and swiping through each step in an intuitive mobile session, just like they are used to with their favorite consumer apps.

This is possible through an end-to-end Digital Completion solution. This one interactive digital experience lets banks share documents with their customers and guide them in real time, every step of the way, until the dispute or regulatory complaint is resolved.

Specifically for advanced dispute workflows, a digital completion platform also provides a clear and trackable audit trail for all required documents shared between the bank and customer, and even any messaging or chat records. Banks can communicate and guide their customers through every step in real time, easing the process for both sides, while gaining a documented engagement channel to assist in resolving the complaint.

Banking & Financial Institutions implementing Digital Completion Results are seeing immediate improvements to key business KPIs, including:

Turnaround Time on individual processes

Improved overall time to resolution

Streamlining all of these aspects of the customer journey eliminates significant time wasted employees time resources on paper-heavy administrative tasks. It also takes needless pain and frustration away for customers, ultimately improving time to resolution that’s especially critical to banking disputes and regulatory complaints.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

Banks want to do better, but their current process just won’t let them: Locking financial institutions into these broken journeys is their dependence on digital silos and legacy processes.

Banks want to do better, but their current process just won’t let them: Locking financial institutions into these broken journeys is their dependence on digital silos and legacy processes.

That’s why these outdated legacy channels are a part of the problem — not the solution — for banks needing to resolve regulatory complaints or any banking dispute process for that matter.

That’s why these outdated legacy channels are a part of the problem — not the solution — for banks needing to resolve regulatory complaints or any banking dispute process for that matter.

Banking & Financial Institutions implementing Digital Completion Results are seeing immediate improvements to key business KPIs, including:

Turnaround Time on individual processes

Banking & Financial Institutions implementing Digital Completion Results are seeing immediate improvements to key business KPIs, including:

Turnaround Time on individual processes