The Pain of Replacement & Additional Credit Card Processes: How Can Banks Take it Away?

By David Abbou

Replacing an existing credit or debit card or getting additional ones issued from your bank or financial institution sounds like a simple and straightforward request — but for many banking customers that process today is still an unnecessarily complex and lengthy one.

There are several reasons why banks receive requests for from customers to issue a new card:

To authorize loved ones on their account and get additional cards issued; or

Simply to replace an existing card due to wear and tear.

While most banks have long-established customer-facing processes for handling these requests, today’s digital-first customers expect to be able to have these requests turned around with omnichannel convenience they’ve grown to expect from e-commerce giants like Amazon and other retail brands they’ll be charging those cards at.

But in 2021, many banks and financial institutions still find themselves trailing behind that digital curve — and that’s currently creating unnecessarily painful journeys for their customers.

Broken Journeys Are Painful Ones for Both Banks & Customers

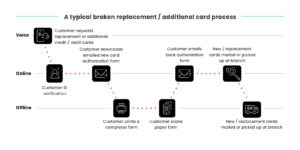

Almost every banking customer has to get a credit or debit card replaced, and probably more than once. Banks and financial institutions want to make processes just like this as quick and easy as possible, but here’s what usually happens.

First, when the customer calls their bank’s contact center, they may already be agitated since they may have just been unpleasantly surprised while trying to make a purchase. We all know how agitating it can feel to be right at the cashier counter of a store ready swipe, buy, and leave, and watch the store clerk repeatedly try charging the credit card in vain before uttering, “I’m sorry but your card simply isn't working, you need to talk to your bank”.

Now, you’ve got an understandably irritated customer calling your contact center, and waiting in line to get an agent on the phone definitely doesn’t help! The agent lets them know their card is simply worn out, but the customer rightfully wants access to their own money and to get a new card ASAP...

But it’s not that simple. The agent first needs to verify the customer’s ID to ensure privacy and compliance. To do this, the agent will ask the customer a common KBA question, such as what was the first school they attended — and a stressed out customer may well not be able to recall the answer…

Next thing you know this frustrated customer is asked to verify themselves in-person at the nearest branch…but it’s 8 p.m. and that branch has already closed for the day. Resolving this relatively simple process today? Not possible. The customer’s frustration understandably boils over.

They weren’t able to make that purchase today, their next attempt to solve the problem with the agent didn’t go smoothly, and now they have to make time to appear at the branch tomorrow, just so they can have access to their money.

Obviously, banks want and need to do better for their customers. But they can’t sign off on a re-issued credit card without sufficiently verifying the cardholder’s identification — that can open up fraud risks and jeopardize the customer’s bank and credit information.

This is just one example of a broken customer journey - forcing banking customers to hop from one channel to another, be it contact center agent, website or portal, or local branch all just to get through the process and receive their new card.

These digitally incomplete journeys clog up staff time and resources handling manual and paper-based admin work, and slow down turnaround times for banks while creating friction for their customers.

It’s this pain that damages customer relationships for banks, risks churn, and hurts key business KPIs such as NPS and CSAT.

Behind this pain are digital silos and legacy processes.

Digital Silos and Legacy Processes Complicate Replacement Credit Card Requests

While banks have invested greatly in digital transformation to internal core systems in recent years, they’ve pieced together their customer-facing journey with multiple point solutions that operate completely in silos.

Using separate siloed systems such as e-signature and ID verification that are not automatically integrated effectively bounces customers from one channel to another, and in many cases not the digital options most convenient to them.

And while banks turn to these solutions to make once manual processes digital, their functionality still depends on legacy formats such as PDF-based forms and documents. Far from intuitive (When’s the last time you tried filling out and signing a PDF form online from your mobile?) These outdated legacy processes defeat the purpose by forcing their customers offline yet again.

Replacing Broken Customer Journeys with Digital Completion

Today, making banking processes like replacement credit cards or additional cardholder requests seamless and hassle-free requires giving customers one end-to-end digital experience that swiftly guides them through the entire process, right on to completion.

Digital Completion technology has now emerged that enables banks to integrate all customer-facing steps into one real-time interactive session. Banks can easily collect digital forms and documents from customers, review reports and supporting documents together in real time, and notify customers once their request for a replacement credit card is approved.

Integrating all eForms, eSignatures, ID verification, and supporting documents into one seamless digital customer experience lets customers complete all of these steps using the digital device that’s most convenient for them.

Creating one unified workflow enables banks to finally deliver a journey that’s digital from start to finish, allowing customers to complete the entire process in the moment from their smartphone.

Clunky PDFs that drive customers needlessly to your contact center or branch? They can now be put in the rearview mirror.

Banks and financial institutions leveraging Digital Completion technology today:

Speed resolution time by 67%

Lift Completion Rates by 25%

Reduce customer journey touchpoints by 60%

Digitalizing replacement or additional card requests for banking customers lets banks resolve replacement and additional card requests quickly and painlessly for their customers — which is at the heart of competing successfully for their business in the long run.

Start Completing at the Speed of Lightico

Instant eSignatures, Payments, Document Collection & More

The most helpful thing about Lightico is the fast turnaround time, The upside is that you are giving your customer an easy way to respond quickly and efficiently. Lightico has cut work and waiting time as you can send customer forms via text and get them back quickly, very convenient for both parties.

"Great Service and Product"

I love the fact that I can send or request documents from a customer and it is easy to get the documents back in a secured site via text message. Our company switched from Docusign to Lightico, as Lightico is easier and more convenient than Docusign, as the customer can choose between receiving a text message or an email.

These digitally incomplete journeys clog up staff time and resources handling manual and paper-based admin work, and slow down turnaround times for banks while creating friction for their customers.

It’s this pain that damages customer relationships for banks, risks churn, and hurts key business KPIs such as NPS and CSAT.

Behind this pain are digital silos and legacy processes.

These digitally incomplete journeys clog up staff time and resources handling manual and paper-based admin work, and slow down turnaround times for banks while creating friction for their customers.

It’s this pain that damages customer relationships for banks, risks churn, and hurts key business KPIs such as NPS and CSAT.

Behind this pain are digital silos and legacy processes.

Creating one unified workflow enables banks to finally deliver a journey that’s digital from start to finish, allowing customers to complete the entire process in the moment from their smartphone.

Clunky PDFs that drive customers needlessly to your contact center or branch? They can now be put in the rearview mirror.

Banks and financial institutions leveraging Digital Completion technology today:

Creating one unified workflow enables banks to finally deliver a journey that’s digital from start to finish, allowing customers to complete the entire process in the moment from their smartphone.

Clunky PDFs that drive customers needlessly to your contact center or branch? They can now be put in the rearview mirror.

Banks and financial institutions leveraging Digital Completion technology today: